I am invested in Ethereum for similar reasons that I am invested in Amazon Web Services, Microsoft Azure, and Shopify. I want to own the platforms that internet businesses are built on top of. One of the reasons I am attracted to these types of platforms is that customer stickiness is very high. When a company has built their business on Amazon Web Services, switching to a competitor is risky, time consuming, and expensive.

Just as important though, the businesses built on Shopify have a vested interest in making Shopify better and more successful. And this same dynamic is seen with Ethereum. Ethereum is by far the most popular blockchain in the crypto economy, and thus has the most projects and people working to make it successful.

[As a quick disclaimer before I go on, the point of this writeup is not to convince readers on the benefits of crypto/web3. If you think crypto is stupid, nothing in this writeup will convince you otherwise.]

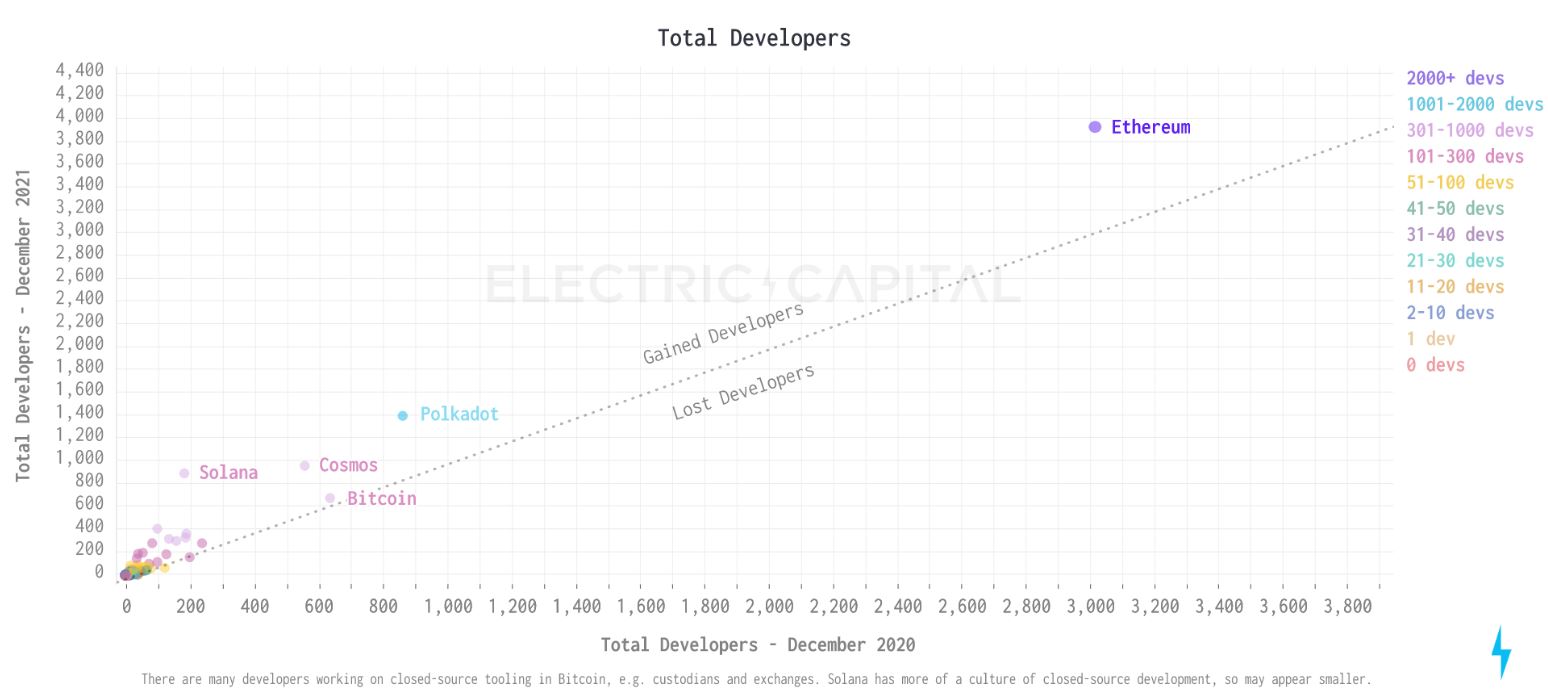

The below chart from Electric Capital shows that dominance that Ethereum has with developers in terms of contributor growth from 2020 to 2021. No other blockchain is even close. Ethereum has the most developers, and they are attracting the most new developers.

In addition to looking at number of developers, there are a handful of other ways to measure market share among blockchains. Total value locked (TVL) measures the value of assets deposited in decentralized finance protocols. Ethereum currently holds 65% of all decentralized finance assets at $72 billion. Binance is #2 with 8% share and $9 billion. Ethereum had been gradually losing market share from 2020 through early 2022 due to so many new blockchains launching. However, Ethereum’s share has increased ~10% just in the past couple months as the downturn and many issues with other blockchains has reminded users how valuable the most secure and most stable chain is.

Of the 17 decentralized finance apps that currently have over $500 million of assets, 15 are on Ethereum. Binance has three, Avalanche has two, and Solana has zero (for those counting, three of the apps are on multiple blockchains).

Ethereum also dominates non-fungible token (NFT) collections. The top 25 collections by trading volume over the past 30-days are all on Ethereum. Out of the top 50 NFT collections, only three are not on Ethereum.

Looking at all types of apps on each blockchain, Ethereum has by far the most volume and activity. Over the past 30-days, Ethereum has 33 apps that have done over $100 million of volume. Binance has 14, Solana has nine, and Avalanche has five.

Next, decentralized autonomous organizations (DAOs) are analogous to limited liability companies (LLCs) but for crypto. Of the 50 largest DAOs in crypto today, 45 are on Ethereum. Solana has the second most with four.

Finally, let’s look at what blockchain makes the most money. Over the past week, Ethereum has earned 11x what Binance has at #2 and 21x more than Bitcoin has at #3. Now, some people might say this is a bad thing: Ethereum is too expensive! I will dive deeper into this below, but for now, I think a good analogy is Apple vs Android smartphones. Apple only sells around 16% of all smartphones globally but creates far more value than the larger Android ecosystem. Apple is a premium product that users pay more for. Likewise, Ethereum has the most secure and most decentralized block space. It is a good sign that people are willing to pay up for that. And if Ethereum has so much demand despite its high gas fees, imagine how much demand there will be when those fees come down significantly over the next couple years.

In summary, Ethereum is by far the most popular blockchain. Ethereum has the most apps and the most users. As seen above, these strong network effects attract the most developers who want to build apps that can connect with other apps and reach the largest audience of potential users. All of these developers are working every day, competing with each other, to make their own apps better—which makes Ethereum better. This results in more apps, more competition between apps, and thus better options available for Ethereum users. This combination of being the largest blockchain with the strongest network effects creates strong barriers to scale for Ethereum’s smaller competitors attempting to catch up.

These network effects are strengthened by the high switching costs of protocols built on Ethereum. For a protocol, the blockchain that runs their app is critical to their business. And those switching costs should increase over time. The longer a protocol uses Ethereum, the more familiar their developers become with it, the more intertwined their app becomes with the Ethereum ecosystem, and thus the more disruptive it would be to switch. Again, this is analogous to AWS or Azure: mission-critical business-to-business software that is used by employees on a daily basis to run the business is very hard to rip and replace. And the more successful a traditional business or a crypto protocol becomes, the riskier it is to switch to a new underlying infrastructure.

Above, I wrote “Ethereum had been gradually losing market share from 2020 through early 2022 due to so many new blockchains launching.” I think it is easy to look at crypto from a high level, see a bunch of blockchains with seemingly little barriers to entry, and conclude that Ethereum cannot have a big competitive advantage. While the barriers to entry for a new blockchain are low, I believe the barriers to scale are much larger. Part of this is the network effects I discussed above, but the other part requires understanding how Ethereum was designed from day 1.

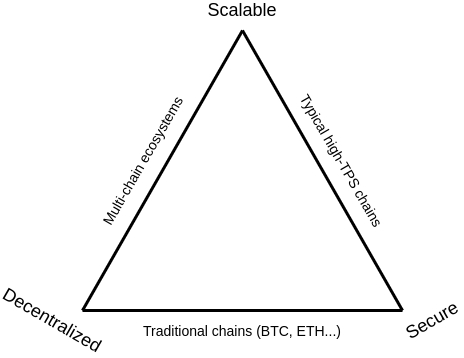

The Blockchain Trilemma dictates that blockchains can only optimize for two of three important properties: decentralization, scalability, and security. Technical limitations do not allow a single blockchain to optimize for all three.

Ethereum was designed to optimize for decentralization and security. Many of Ethereum’s problems are directly related to this design decision. By not optimizing for scalability, the Ethereum network can be slow and expensive to use when congested, which has become the norm since early 2021. However, Ethereum is on the verge of becoming the first fully modular blockchain over the next couple of years.

Transitioning from a proof-of-work chain to proof-of-stake will increase the decentralization and security of Ethereum. Specific hardware will no longer be needed to validate the Ethereum blockchain—ETH tokens and any internet-connected computer will do.

Next, rollups are basically a way for Ethereum users to pool their activity together to get discounted gas fees. Rollups make transaction executions on Ethereum modular, so that transactions no longer have to be done directly on Ethereum mainnet. Rollups built on top of Ethereum will be able to process transactions faster and cheaper than directly on the main chain.

Finally, sharding splits Ethereum’s massive and ever-expanding database across many shards, as opposed to all data being on one monolithic blockchain.

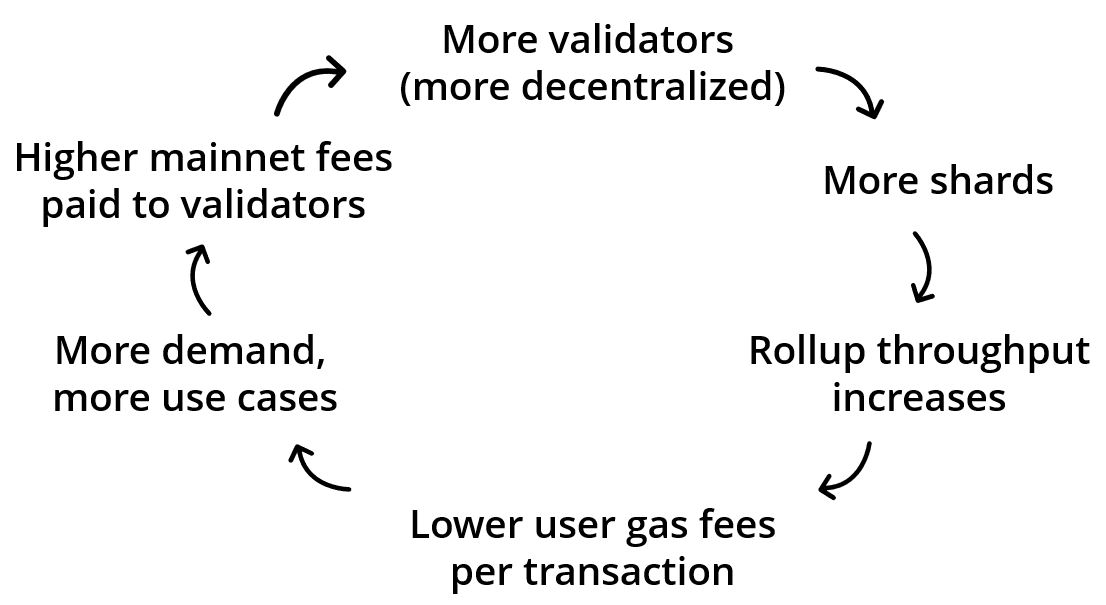

Importantly, the above three changes all reinforce each other. Validating a proof-of-stake network requires no specific hardware, so the number of validators should increase significantly. When sharding is implemented, more validators mean more shards can be supported (as each shard needs validators). More sharding will mean rollups can execute more transactions because all rollups will not be settling to the same Ethereum main chain—they will settle to many shards.

As the scale of rollups increases, they will be able to handle more transactions and execute them faster. More transactions through the same rollup will drive gas fees per user transaction down. This is how micro-transactions valued at a penny or less can someday be viable on Ethereum. Driving down gas fees for users should substantially increase the activity and use cases operating in the Ethereum ecosystem. And more activity and more total fees funneling back to the Ethereum mainnet will mean more people want to be validators to earn a portion of those fees. And the flywheel continues.

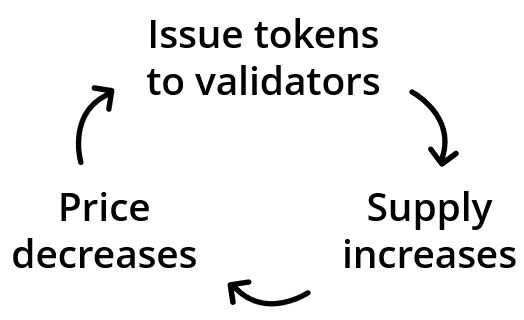

Next, let’s talk about Ethereum’s fees. All blockchains require third parties to validate and approve transactions. These validators have to be paid. If a blockchain charges sufficient fees per transaction, like Ethereum does, validators can be paid from those fees. However, if a blockchain does not charge sufficient fees, then validators are paid by issuing them native tokens of the blockchain. This is when problems arise.

By paying for network security via issuing tokens, more token supply leads to a decreasing token price over time. A lower value network token means more tokens need to be issued for security. This is a vicious cycle.

On the other hand, Ethereum block space is at a premium, and Ethereum charges handsomely to use it. Those fees partially will go to pay proof-of-stake validators. Having a healthy fee market means Ethereum does not have to inflate its token supply to pay validators, which means the supply of Ethereum tokens stays lowers. Less supply means Ethereum’s price will be higher than it would be if its security was paid via issuance. High fees and a scarcer token add to Ethereum’s monetary premium.

ETH that is more valuable incentivizes more people to buy ETH and stake it, which decentralizes the network more and feeds right back into the above flywheel of Ethereum’s coming modular infrastructure. More validators result in more sharding, which means more rollups, which means lower fees for users and thus more demand. More activity means more fees to Ethereum and then more people wanting to buy ETH and stake it to earn a portion of those fees.

Importantly, when I talk about high fees in this discussion, I am referring to the main Ethereum chain, which most users will not be using in a few years. Users will pay very low fees on rollups, and rollups and other large entities that operate directly on Ethereum will pay the higher mainnet fees.

This entire Ethereum flywheel is rooted in one of the core tenets that Vitalik founded Ethereum on: decentralization. Ethereum has designed a modular infrastructure that will be more scalable and faster and cheaper and more secure the more decentralized it becomes.

With that being said, Ethereum is not the only blockchain pursuing a modular architecture. Many of their competitors are starting to realize that a single, monolithic blockchain that tries to do everything will not be able to compete in the future.

However, Ethereum is far more popular than any other blockchain, and Ethereum is also the furthest ahead in developing rollups and sharding. I think the barriers to catch up to Ethereum are large, which is why I am not convinced of the popular “multi-chain” theory—the belief that there will be several (or many) large blockchains that people and applications use. Ethereum is already the most decentralized and most secure blockchain. And soon it will be the most scalable. I think it is very possible that blockchains end up being winner-takes-most.

Flows, supply and demand, and valuation

Everything I have written up to this point is why I initially invested in Ethereum. I want to own the underlying platform that powers the decentralized internet. Moving on from Ethereum’s fundamentals, I now want to look at how supply and demand for ETH is changing. While I want to own ETH for the long-term either way, I do think there are some intriguing catalysts that might move its price over the next 1-2 years.

In the next few months, Ethereum is expected to switch from being a proof-of-work blockchain to proof-of-stake. The implications of this are enormous.

Currently, the Ethereum blockchain is validated by miners—many of which are professional mining companies that rent warehouses, own servers, have employees, etc. The revenue for these mining companies comes in the form of ETH that is issued to them in exchange for their service. However, most of this ETH gets immediately sold so they can pay their real-world business expenses—like rent, salaries, new servers, and lots of electricity.

When Ethereum switches to proof-of-stake, validating the network will be simpler and does not require those real-world expenses. This has two major benefits. First, around 70% less ETH will need to be issued to pay for validation. Second, stakers validating the network will not need to sell the ETH issued to them to pay for business expenses. Thus, daily sell pressure from validators is expected to be significantly less than it is currently.

With that being said, less ETH being issued and less of that issuance being sold will still only amount to <1% of daily ETH volume. That might sound meaningless, but I don’t think so. A large portion of ETH volume is price insensitive trading from entities like exchanges and quant funds. I believe a small decrease in selling every single day can have a meaningful effect on price at the margin over time. And there are two other factors that are helping this supply and demand dynamic.

After the merge, people who stake ETH tokens will receive their proportional share of fees generated on the Ethereum network. Staking ETH will be equivalent to investing in a stock and receiving dividend payments. Due to everything I described in the first half of this writeup, I believe the yield earned on staked ETH will become the risk-free rate of crypto. My guess is that this yield settles around 3-5%.

Currently, there are 121 million ETH tokens outstanding and 13 million of those are staked. The current yield on staked ETH is 4.2% but that is expected to meaningfully increase after the merge (for reasons that are unnecessary to explain here). For the yield to eventually settle at 3-5% will require much more ETH to be staked—probably around 30 to 50 million total. This would mean another 17 to 37 million ETH that is staked and not being traded.

Finally, despite the current investing environment that is terrible for just about everything, I believe the demand for owning ETH is going up over the long-term. More traditional brokerages are offering Bitcoin and Ethereum trading. More institutional investors have shown interest in owning Ethereum. I believe things like index funds that own or track Ethereum are inevitable. And this institutional demand should only increase when they can own a profitable and growing tech platform that pays them 3-5% on their investment each year.

So, in summary, I expect demand flows for Ethereum to be increasing over the next year or two just as structural selling and the amount of unstaked ETH that is being trading are both decreasing. Ultimately, the price of any asset is determined by supply and demand, so demand increasing at the same time that supply decreases is a potentially powerful combination.

Having said all that, valuation is difficult. I have seen plenty of investors try to value Ethereum and quite frankly, not a single one has given me much confidence (though I appreciate those people sharing their thoughts publicly and I have still learned from them). The thing that I struggle with is the scaling of Ethereum’s layer 2 ecosystem of rollups and sharding.

Rollups and sharding should increase Ethereum’s speed and decrease fees by orders of magnitude for the end users. The hope is that these decreased fees per transaction are more than made up for with more transactions. I think this makes sense, but the magnitude of that is a complete shot in the dark for me. Will decreasing fees 90% increase usage 10x? 100x? I have no idea. I think it is possible that Ethereum is successful and yet the fees decrease so much that the chain is not as profitable as some people are discounting the future at today.

On the other hand, there is a legitimate argument that rollups will not cause fees paid to Ethereum to drop at all. In the future, you and I will probably not be doing transactions directly on Ethereum mainnet. Our transactions will happen on rollups and then the rollups will settle and pay fees on Ethereum. Other groups using Ethereum mainnet could be companies, institutions, and governments. If this happens, the entities paying Ethereum fees are going to evolve from price-sensitive individuals today to price insensitive organizations in the future, and thus maybe the fee decrease is not as much of a concern as I think.

How all that will shake out, I do not know. But I do think slapping a multiple on Ethereum’s current earnings or extrapolating the current numbers forward are both overly simplifying things. In my opinion, there are too many moving pieces over the medium-term for that. I do not have a better method though. If I was more confident in how to value Ethereum, it would be a larger position for me. Although to be fair, looking at simple methods like current multiples do not show a demanding valuation.

I am optimistic about crypto’s future, and I am optimistic that Ethereum has a good chance at being the settlement layer for the decentralized internet. But I think valuing Ethereum today is a bit like valuing the internet in 1995 or valuing the iPhone in 2007. If Ethereum is successful, the most popular apps built on it are difficult to even imagine today because they cannot yet exist with today’s technology. Ethereum’s merge this summer and the layer 2 buildout over the next couple years will mean the majority of the foundational infrastructure for crypto will be in place for the first time. And finally, we will be able to see its potential.