Burford Capital is the largest legal finance company in the world. While Burford is mostly known for funding lawsuits, they provide legal capital in a variety of ways. In the simplest example though, Burford funds a plaintiff’s lawsuit by paying their legal expenses. If the case is lost, Burford loses their entire investment. If the case is won, the plaintiff pays Burford a share of the winnings. I believe there are numerous benefits for plaintiffs to get funding from a company like Burford.

At a high-level, litigation funding can flatten the legal playing field. Lawsuits are expensive. Many legitimate lawsuits are never filed because the potential plaintiff cannot—or does not want to—pay for the legal expenses. Plaintiffs often do not like the traditional hourly billing model that many law firms operate on. But working with a litigation funder allows a plaintiff to exchange having to pay their own legal expenses for a percentage of their winnings if the case is victorious. To date, many plaintiffs have welcomed this trade-off of less downside, less upside, and more flexibility.

In addition, much of Burford’s client base is large corporations, many of them public. For corporations, legal costs are expensed immediately and usually fall under selling, general, and administrative expenses on the income statement. Litigation funding allows corporations to move legal costs off their financial statements, decrease operating expenses, invest that cash elsewhere, and still benefit in most of the upside.

Finally, Burford has a lot of knowledge that can be valuable to a legal team. Burford has been in business since 2009 and they have been involved in well over a thousand legal claims. They have been successful by being picky in the cases they choose to fund. If Burford wants to invest, this adds an element of independent validation to a plaintiff pursuing a claim. And the plaintiff’s chances of winning can increase by having Burford’s expertise on their side.

In addition to being a win-win for Burford and their clients, I also believe Burford has a strong advantage in this burgeoning industry. By my estimate, Burford has around 30-40% market share and is more than twice the size of the second largest litigation funder, Harbour Litigation. It is difficult to get more precise numbers because most competitors are private and, as the industry is relatively young, there is not much independent third-party data available.

Nonetheless, this scale results in several advantages. First, Burford has little competition in the largest deals. Their market share may be 30-40% of the overall industry, but I suspect as deal size increases, Burford’s market share rises to a large majority. Burford’s average investment is over $20 million dollars, and their largest to date was $200 million. Except at the fringes, a small litigation funder with $300 million in total capital does not compete much with Burford.

In addition, I believe that by focusing on the high-end of the industry, Burford attracts customers that are less price sensitive and care more about pedigree and relationships. A corporation pursuing a claim worth potentially tens or hundreds of millions of dollars is unlikely to just default to working with the lowest bidder. I believe Burford has many traits that make them the safest partner for law firms and corporations to work with.

As stated, Burford has by far the most scale and capital in this industry, which means they have the least concentration risk. It is riskier for a plaintiff to accept $20 million dollars from a $300 million-dollar fund vs Burford that has over $4 billion in total funding. Burford also has audited public financial statements, permanent capital, and major institutional investors.

Having the most scale means Burford has the most experience and data of any litigation funder. Because of this, Burford is often a strategic partner as opposed to merely a transactional one. This matters the most in the high-end space where Burford focuses. I believe smaller litigation funders are more likely to fight over smaller deals with lower quality clients who are more price sensitive.

Decades ago, the saying “nobody gets fired for buying IBM” became popular. This was because IBM had a good reputation in technology and a recognizable brand name. While purchasing technology from a small, unknown competitor may be risky, a purchasing agent at a company knew they would not be blamed if they bought IBM—even if something went wrong.

In legal finance, Burford is comparable to IBM. Burford is the largest company in the industry, and they are the only one with a recognizable brand name. I realized this when I was researching the industry and noticed how many news stories mention Burford and no one else. Even competitors cite Burford for industry data.

This brand name recognition has resulted in Burford being the thought-leader in this industry and thus more likely to be the default option when a plaintiff is looking for funding. With the market share that Burford has, they have become synonymous with litigation funding.

The best part is that these benefits reinforce each other, which is why scale can be such a powerful advantage. Because Burford is the largest funder, they are often the default choice for legal finance. This results in them getting more free marketing than their competitors. Free marketing lowers their customer acquisition costs by attracting customers cheaply—which leads to more scale.

As Burford’s scale increases, so does their reputation and pedigree. This helps them attract the high-quality law firms and Fortune 500 companies that they want to work with. Finally, the funder with the most scale sees the most deals, funds the most cases, has the most data, should be able to price their investments most accurately, and thus is the best partner for plaintiffs—which leads to more scale.

The future legal finance industry may be comparable to venture capital. Legal finance is not a winner-takes-most industry, but the largest and longest-running venture capitalists have advantages over small, lesser-known players. Of the top ten venture capitalists, Andreessen Horowitz is the newest firm at 12 years old—with eight of the top ten being 20+ years old and three being founded over 40 years ago. Reputation and size matter in these types of industries and being in business a long time helps with both. And as I described above, reputation and size reinforce each other. There is some evidence of this in the legal finance industry as the top firms were all founded in the late 2000s when this industry was just getting started.

It is difficult for small litigation funders to catch up to Burford because there are barriers to scale in this industry. If a lawyer launches a new fund with $300 million and invests it all within one year, it would be another two to three years before a meaningful portion of those cases have concluded. At that point, three years after launching, there may be enough evidence that the fund knows what they are doing and thus is able to raise $600 million more. Three more years and maybe they are able to raise $1 billion. At that point, their total assets could be $2.5 billion or so.

To put that in comparison, Burford ended 2020 with over $4.4 billion in their total portfolio. And Burford would continue to scale as this theoretical new fund launches and grows. So, at a minimum Burford is six years ahead of this new fund even approaching Burford’s current scale.

Raising capital, investing that capital, waiting for lawsuits to conclude, and raising more capital takes many years. There is no way around that. Because of this scale advantage, it will be difficult for other legal funders to catch up with Burford’s size and reputation.

In addition to benefitting from the barriers to scale in this industry, Burford also has captive customers. The relationship between Burford and a corporation is a long one. The average case that Burford invests in takes two to three years to come to conclusion. But that is just the average. Burford still has open cases from 2010. If a case does not settle, it is not uncommon for a trial and appeals to take 5+ years.

Thus, if Burford invests in a book of cases for a company, they are probably going to work together on a regular basis for many years. If the relationship is comfortable, that client is more likely to stick with Burford for future funding needs. For that company, the process to get additional funding with a funder they already work with is quicker and simpler than finding a second funder to bring in.

The above is true because there are search costs when it comes to finding a funder to work with. Search costs arise when it is difficult to compare offerings between competitors. Insurance is a common example. Insurers have different terms and conditions that can radically change the outcome for customers. Likewise, it can be difficult to do an apples-to-apples comparison between different legal finance companies as there is an infinite number of ways to structure deals.

In addition, this is not an industry that lends itself to open RFPs. A lawyer would be acting recklessly if they put out an RFP that contains intimate details of their case to every third-party funder in the industry. Burford has discussed before how the RFPs they partake in usually only have a couple companies participating.

Even better, repeat customers generally come straight back to Burford without doing an RFP. As evidence of this, 70% of Burford’s new clients have historically become repeat customers. But I believe Burford’s retention rate could actually increase going forward. Over the past few years, Burford has been expanding its business beyond their core of litigation funding.

“This continuing evolution in Burford’s business requires investors to think of us more broadly as a specialty finance company… and not just a litigation funder.” – Burford Capital 2018 Annual Report

Burford wants to be the go-to capital provider for whatever the legal industry needs. And the more services Burford offers, the more ingrained Burford becomes in their customers’ businesses. This means stickier relationships and increased switching costs for those clients.

This is a common strategy of many successful businesses: create sticky customer relationships and then cross-sell those clients on tangential products or services. This can be an efficient way to increase customer retention and average revenue per customer.

Management and culture

Chris Bogart, CEO, and Jonathan Molot, Chief Investment Officer, co-founded Burford Capital in 2009. It should not be a surprise given they are both very successful lawyers, but it is refreshing to hear how rational and well-spoken they are. They come off as intellectually honest without any bullshit. Chris is probably the most anti-guidance public CEO I have come across. He does not answer questions that even remotely resemble attempting to predict the future.

“as corporate litigators we have spent decades of our professional lives seeing, and dealing with, the misjudgments and other fallacies of corporate executives and market participants. We were the people called in when companies got into trouble… This experience leaves us skeptical about predictions and deeply reluctant to try to make them… Our view is that it is our function to be excellent stewards for shareholders’ capital and to provide investors with data and with commentary on the past, and that it is for investors to form their own individual views about what the future holds.” – Burford Capital 2017 Annual Report

Analyzing culture is important for any company I want to potentially invest in, especially so for Burford. Their business boils down to generating good returns from funding lawsuits. Thus, for me, the crux of investing in Burford was: do I trust the founders have created a culture that can sustainably invest capital at high rates of return? I believe Chris and Jonathan have.

The most obvious proof of this is their results. Looking only at their core balance sheet investments that have concluded, Burford has generated a 66.9% return on invested capital and 24.9% IRRs (and these numbers exclude their most successful investment that is still ongoing). Historically, that is fantastic, and it is pretty good evidence that they know what they are doing, but what matters to me today is if they can continue to generate good returns going forward. When considering this, I appreciate that Burford has such a structured process with checks and balances for approving and making new investments, releasing payments, and for portfolio management.

“Before we make a commitment, we conduct extensive in-house due diligence. All financing transactions must be approved by our dedicated Commitment Committee which considers legal merits, risks, reasonably recoverable damages, proposed budget, proposed terms, credit issues and enforceability.” – Burford Capital 2020 Annual Report

“We have built proprietary analytical tools that enhance our ability to analyze and price any legal finance matter. Using the significant data set we have developed over 11 years of operation as well as the views of our experienced underwriters, we employ a bespoke asset return model to calculate the likelihood of loss and probability-weighted risk-adjusted returns for each opportunity considered by the Commitment Committee.” – Burford Capital 2020 Annual Report

“for any payment, regardless of size, to be released, that payment must be created within the banking system by one of several team members, none of whom have the authority to release payments, and then the payment’s release must be authorized by two other team members separately, neither of whom is able to create a payment. Thus, at least three different people from two different groups are required to provide sign-off before a single wire payment leaves Burford’s account. Moreover, payments are not created without a formal process of approval, with capital provision asset payments being circulated widely among and approved by the underwriting team. Senior executives in the business, including the CEO and the CIO [the co-founders], do not have access to our payment systems and cannot create or release payments as a control matter.” – Burford Capital 2020 Annual Report

“Each of our matters has a Burford professional assigned to monitor the underlying case. We generally schedule regular calls with clients to discuss case developments. Case updates are reported monthly to senior management. We also conduct a quarterly risk review and provide an in-depth quarterly report on our entire portfolio to senior management and our Board. We conduct an extensive semi-annual review of every legal finance asset for valuation purposes.” – Burford Capital 2020 Annual Report

Burford funds its investments in three different ways: equity from the public company balance sheet, debt, and outside capital in the funds that Burford manages. Each of these sources has pros and cons. Investing directly from the balance sheets means Burford’s shareholders get all of the upside, but this cash is limited. If Burford only had access to their own equity, growth would be slower. Using debt and outside capital allows Burford to invest more capital, but that also gives up some of the upside. In this regard, interest expense on debt is cheaper than outside capital where Burford only earns management and performance fees. However, debt levels must be managed as to not cause risk to the overall company.

Burford refers to these three sources of capital—balance sheet, debt, and outside capital—as the three legs in their capital stool. Management often discusses on conference calls and in their semi-annual reports the balancing act of optimizing the pros and cons of those three legs.

“Our funding sources [are organized] by expected return, risk, and life of the assets we originate. We use our balance sheet and certain dedicated funds to provide capital for higher risk, higher return, longer-lived assets such as those created in our legal finance business. We typically use dedicated funds, in which our balance sheet is an investor, to provide capital for the kind of lower-risk, lower-return, shorter-lived assets that typify complex strategies activities. And we use still other dedicated funds (without balance sheet investment) for low risk, low return, very short-lived assets, such as post-settlement and law firm receivables financing.” – Burford Capital 2020 Annual Report

“In planning [our debt] issuance, we have purposely constructed a set of laddered maturities with an overall weighted average maturity [4.4-years] well in excess of the expected weighted average life of our legal finance assets [2.3-years]. We have also sized these issues so that any single year’s maturity amount is significantly less than our historical annual rate of legal finance asset realizations, which we believe protects against a liquidity shortfall when these bonds become due should we not refinance them.” – Burford Capital 2020 Annual Report

Just as important as how the company and sources of capital are structured is employee incentives. Humans are—understandably so—selfish creatures. One of our most basic instincts is to do what is in our own best interest. Because of this, I believe creating incentives that encourage employees to do what is both in their own best interest and the long-term interest of the company is one of the most important things a founder does.

With Burford, one of the key elements of their employee performance compensation is that it is based on cash generation. An unfortunate requirement of Burford’s accounting is fair value adjustments. When they release results, a meaningful amount of their “income” is from marking up what they think the fair value is of their investments. This can add subjectivity to their results, though I believe Burford has released significant evidence supporting their conservativeness in marking up cases. Importantly, Burford’s employee compensation does not incentivize them to aggressively markup cases.

“We do not include non-cash metrics like fair value in our compensation assessments… our general compensation philosophy is team-based rather than individual as we believe that investing in this asset class benefits from a team approach and not assigning individual ownership of and responsibility for individual investments.” – Burford Capital 2019 Annual Report

Finally, equity ownership is high throughout the company. The two co-founders have large positions as expected, but they have also each bought several million dollars more of stock over the past two years. In addition, each co-founder has $2 million invested in Burford’s funds and $500k in Burford’s publicly traded bonds.

In 2017, when their Strategic Value Fund was launched, management mentioned that Burford employees as a whole invested over $5 million dollars. In 2019, it was mentioned that “dozens” of employees are invested in Burford’s funds (which is meaningful given their total employee base was only 129 at yearend 2019). Also, Burford’s directors have $1.5 million total invested in the funds and they own $1.05 million in bonds, plus several million in stock. While the new directors are yet to be as invested, one of the directors who joined the board last year did invest $250k into Burford’s new debt offering just a couple weeks ago.

New employees get granted equity and current employees get annual grants—all of which cliff vests after three years. And when employees choose to participate in Burford’s deferred compensation plan, the company match is in Burford stock. In addition, all senior management, not just the co-founders, are required to hold Burford stock worth at least 3x their annual base salary.

All of this results in a culture that is heavily incentivized by Burford’s stock performance over multi-year periods and the company’s ability to generate cash on its entire portfolio. I pulled many quotes from Burford in this section to give it straight from the horse’s mouth, but there are many more interesting discussions of their culture in the semi-annual reports, conference calls, and interviews the co-founders have done.

In very simple terms, the success of any business is determined by their ability to allocate capital. A company sells something, earns revenue, and then invests that capital however the leaders and culture best see fit—hiring employees, marketing, a new office, R&D, investments, etc. The companies that invest money at the highest rates of return for the longest periods of time are the most successful. This is why I am often attracted to companies like Burford Capital that have capital allocation ingrained in their company culture.

“Burford is fundamentally a business run by experienced lawyers… The challenge in many businesses is reining in individuals who take on unacceptable risk, and it is the function of the lawyers to hold those reins. At Burford, we have a business run by people accustomed to that role. Burford’s culture is a disciplined, risk-focused one, augmented by an eight-member in-house legal and compliance team… We take risks in order to provide attractive returns to our investors. This means that risk management has to be embedded in everything that we do.” – Burford Capital 2019 Annual Report

Is Burford Capital a black box?

Of the many investors I have talked to about Burford, well over half have said it is a black box. When I hear the phrase “black box”, I think of a business like an investment bank that takes both sides of a wide variety of bets, many of which are on margin. The result is an extreme difficulty in estimating future cash flows because there can be unknown underlying correlations in those bets that make large negative events possible.

I do not believe Burford fits that definition. To be fair, Burford is not the simplest business I follow. But I think it is simpler than a lot of investors realize. Burford funds the legal expenses for large lawsuits, and then waits a few years (on average) for those lawsuits to conclude. If the lawsuit is lost, Burford loses their entire investment. If the lawsuit is victorious, Burford shares in the winnings. The range of assets that Burford invests in is significantly narrower than the types of businesses I would label as black boxes. Burford is not investing in obscure things and, importantly, they are not acting as banker for others to make obscure bets against.

I struggle to see how funding lawsuits on the large and diversified scale that Burford does could blow up on them in the way that Credit Suisse recently experienced. In my opinion, that is the concern when investing in a black box financial—the company is taking both sides on a ton of very complicated bets with unknown correlations. That is not Burford. If Burford invests $10 million in a lawsuit that fails, they cannot lose any more than that $10 million.

Importantly, Burford is well aware of the value of diversification with respect to avoiding too many lawsuit investments that could be correlated. Starting on page 47 of the 2020 annual report, Burford spends four pages walking through various potential concentration risks in their portfolio: geography, currency, case types, industries, corporations, law firms, and related claims. I think a few of these are worth paying attention to.

As of yearend 2020, Burford’s largest corporate client accounts for 4% of Burford’s groupwide commitments. While their largest law firm accounts for 12% of groupwide commitments, that business is spread among more than 50 partners at that law firm litigating over 40 different lawsuits. Finally, the balance sheet’s largest concentration is 19 related lawsuits that account for 9% of deployed dollars. None of these numbers concern me. Burford updates these and other concentration numbers every six months, and they have discussed the value of diversification many times. I do not get the impression that concentration risk is something that gets overlooked at Burford.

Now, to zoom out a bit, I do think all public companies have some black box element to them. As a small outside investor, it is impossible for me to understand everything that is going on inside a public company. Executives and many midlevel managers understand the inner workings of the companies I invest in better than I ever will. This is exactly why I put so much emphasis on trusting the founder, learning about what culture they have created, and what actions their employee compensation incentivizes.

In my mind, Burford’s “black box-ness” is similar to Constellation Software’s. I would be lying if I said I follow or understand the hundreds of $5-million-dollar acquisitions that Constellation Software has made. In the aggregate, however, I do understand Constellation’s investment philosophy, their competitive advantage, and I believe there is substantial evidence that Mark Leonard has created an amazing capital allocation machine. Likewise, that is how I think about Chris Bogart and the culture of diligent capital allocation he has created at Burford Capital.

Financials and valuation

Burford is often compared to venture capital—I made the analogy myself when discussing the reputation advantage Burford has from being the largest and one of the longest tenured legal finance companies. However, I think this analogy gets misconstrued by investors sometimes.

The old adage of venture capital is they lose money on most of their investments, a handful are moderate successes, and one or two huge winners provide the vast majority of profits. Burford has a better track record than that. Looking only at completed balance sheet investments through the end of 2020, Burford has lost money on 32.4% of their investments. However, looking at the actual dollars deployed, only 15.4% of Burford’s cash deployed has gone into investments that eventually lost money. Either way you look at it, most of Burford’s investing makes money.

Continuing to only look at these same completed cases, Burford’s total return on invested capital to date has been 66.9%. If you remove their three most successful completed investments, their return on invested capital is still 47.3% (and again, these numbers already exclude Burford’s most successful investment that is still ongoing). I believe the health of Burford is not dependent on one or two homeruns like many investors seem to think.

With that being said, I do understand why many investors get the wrong idea of Burford’s business if they only take a quick glance. Out of all the companies I follow, Burford’s financial statements are the least helpful in terms of trying to understand the business and how it is performing. There are three reasons for this. First, Burford does not control the vast majority of the lawsuits they invest in. Burford cannot choose to settle a bunch of lawsuits just to improve short-term results. Because of this, it is inevitable that results are lumpy. Some periods will have lots of lawsuits come to conclusion and other periods will have very few. Thus, looking at something like year-over-year revenue growth usually is not a good signal as to how well the business actually performed.

“As we have long made clear, we can neither predict nor control the timing of the generation of litigation returns. We finance large, complex commercial claims. Our realizations come from their resolution. There is no ‘normal’ for such claims; they are inherently idiosyncratic. We have had cases resolve in less than a week, and we have matters from 2010 still going strong. That is the opportunity in our business, and it is why we are able to generate the returns we have historically delivered.” – Burford Capital 2020 Annual Report

Second, Burford currently manages eight investment funds. For six of these funds, Burford is the manager and collects fees for doing so, but that is it. However, Burford is both manager and a minority investor in two funds. Being an investor means those two funds’ entire results are consolidated into the financial statements.

Third, Burford is required to make fair value adjustments for their investments when they report earnings. This is helpful to see how investments are progressing, but it muddies the financial statements from what I care most about—how much actual cash Burford generates.

To understand the overall scale and growth of the company, I focus on total groupwide commitments. This includes the balance sheet and the eight funds they manage. This is how many dollars Burford as a whole is committing to new investments. Looking at the individual sources of where new commitments are being made is also important, but those numbers can be lumpier. Importantly, Burford has objective rules and formulas for where new investments are made from (which are discussed in their reports), so it is not based on subjective decisions. Nonetheless, when a new fund is launched, it may see increased investment for a couple years, which momentarily takes investments away from other areas. What I care about here, though, is Burford’s overall scale. Let’s look at those numbers.

That looks like a business that plateaued from 2017 to 2019 and then collapsed in 2020. However, there are two important points. The first is that Burford made its two largest investments in its history in 2017—one for $200 million and one for $150 million. Portfolio deals that large are fantastic for Burford, but there are only so many of those opportunities in the entire world. I expect nine-figure investments to come around once in a while and I will be happy when they do, but they do create lumpiness. Removing those two investments results in a chart that tells a different story.

That looks like a business with much steadier growth from 2015 to 2019, though 2020 obviously sucked. Especially during the peak of COVID, many courts and lawsuits came to a complete halt. Burford’s business slowed significantly in 2020, but especially in the first half. As 2020 went on, courts transitioned to operating remotely for the most part, though some delays throughout the industry are still present. Total groupwide commitments in H1 2020 were down 74% year-over-year, whereas H2 was down 32% (and up 189% sequentially). Before COVID, I would not have been excited about those year-over-year numbers, but H2 did show a very clear improvement from H1. And as I will get into here soon, I am confident this trajectory will improve into 2021 and beyond.

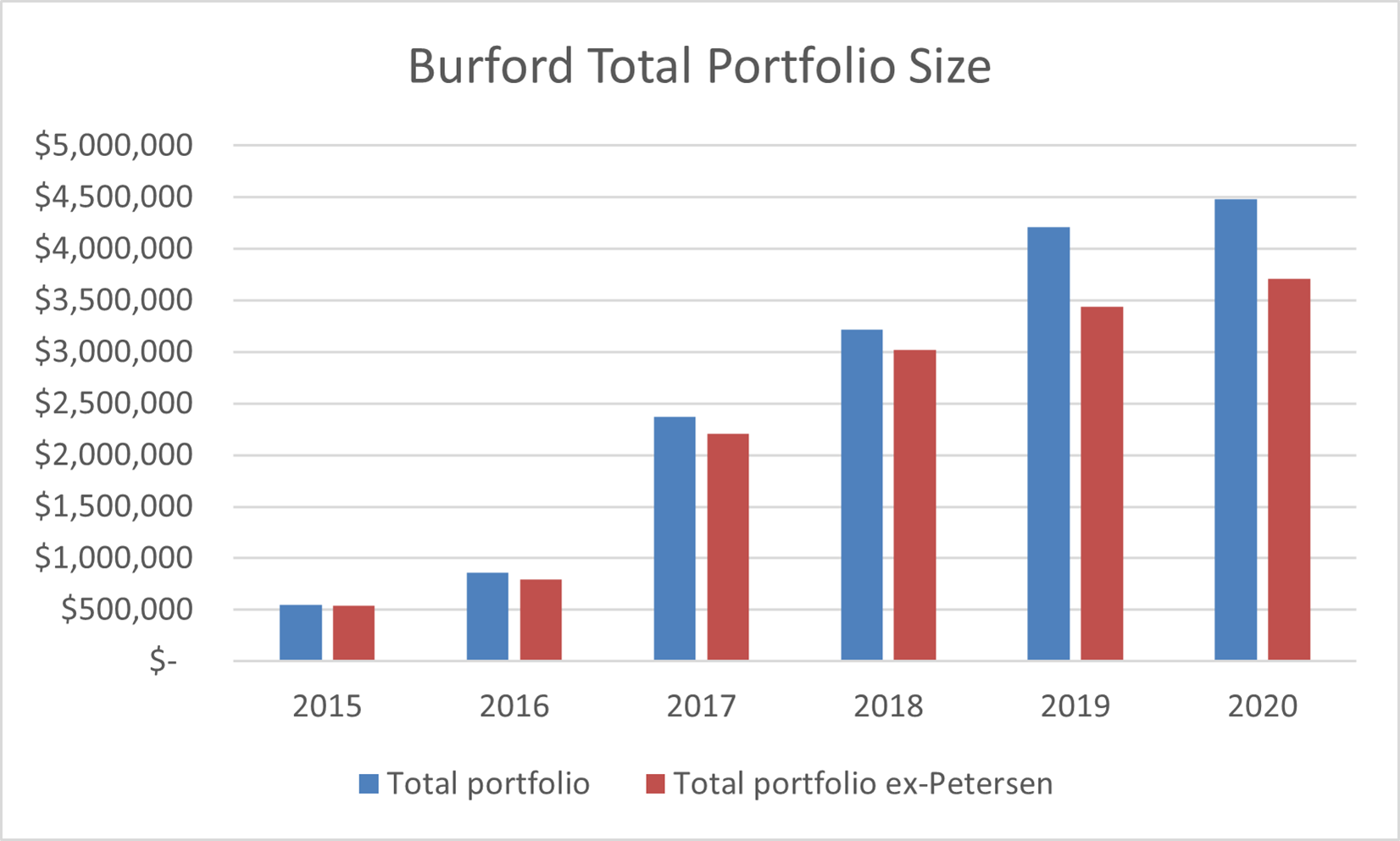

Another way to look at Burford’s overall growth is to look at their total portfolio over time. Whereas the above charts show how many investments Burford makes per year, portfolio size looks at commitments made plus fair value markups. This shows us how Burford’s investments are progressing and what kind of profits we can expect from them in the future.

Petersen is Burford’s largest investment that I will go in depth on below (Petersen’s carrying value for 2015-2018 are my estimates, 2019-2020 numbers are from management). Nonetheless, this chart shows Burford’s total portfolio has steadily grown every year. And I expect that progression to ramp up in the near future after a slower 2020.

With that in mind, let’s talk valuation. I am going to walk through the key assumptions for my discounted cash flow and explain what financials I pay most attention to as I go. I think of Burford as two segments: investments made directly from the balance sheet, and investments made through the funds they manage. The balance sheet investments are where most of Burford’s value lies. Burford generally refers to this as “Burford only”, “balance sheet”, or “direct.” This is the core business where Burford uses equity and debt from its balance sheet to make direct investments into legal assets, mostly lawsuits.

To analyze this part of Burford, I focus on the returns generated from completed cases and how many dollars they deploy to new cases. I focus on completed cases because I prefer to ignore the non-cash fair value markups. I want to see the actual cash returns they generate. If Burford continues to deploy a significant portion of their cash flow into new cases at attractive returns, the company is increasing its value. That is what I care about. On Burford’s investor relations website, a file can be downloaded that shows investment data for every completed investment they have made. And page 54 of the 2020 annual report shows how many dollars their balance sheet has deployed to new cases.

In 2020, Burford’s balance sheet directly invested in $225 million worth of legal assets, but I believe that number is going to meaningfully increase going forward. Burford is already seeing, and is expecting to continue seeing, an increase in demand for legal funding come out of COVID. Bad economic periods generally result in bankruptcies, cancelled partnerships, and broken contracts. With this in mind, there were several statements from Burford’s 2020 earnings that stuck out to me.

“this reminds us of the period of opportunity for Burford that existed after the global financial crisis, as we spent some number of years litigating some cases in that area. This isn’t necessarily business transformative, but it’s business additive, and it’s something that we expect to see going forward for a number of years.” – Chris Bogart, 2020 earnings call

“given the medium-term potential we see to originate attractive capital provision-direct assets, we would rather deploy incremental funds into those higher returning assets rather than make new commitments to capital provision-indirect assets” – Burford Capital 2020 Annual Report

“Our Groupwide portfolio stands at $4.5 billion, five times larger than at the end of 2016. That new business will take time to turn into cash profits, but if history repeats itself, it will do so reliably over the years to come—and we intend to continue adding to that portfolio every year, in scale.” – Burford Capital 2020 Annual Report

“return to the debt markets given the level of future demand we anticipate for our capital” – Burford Capital 2020 Annual Report

Shortly after their 2020 earnings, they announced a new debt raise of $400 million. In summary, I think Burford is expecting a multi-year period of high demand for their services. But beyond benefits from COVID, I think this industry has a decade+ of healthy growth ahead of it. Below, Burford discusses their tangible addressable market.

“The challenge is distilling the global pool of legal fee spending and claim value—which is almost unimaginably enormous—into the portion of that pool that is theoretically addressable by us and doing so without history to guide us. We do know that each year (i) vast amounts of money—hundreds of billions of dollars—are spent globally on legal fees and (ii) vast numbers—probably millions—of litigation claims and other matters involving legal or regulatory risk come into being and that hundreds of billions if not trillions of dollars change hands in resolving those claims. But we have no data to enable us to project what proportion of the total legal pie we and our competitors could occupy in the future except to say that we are not worried about market saturation—quite the opposite. Our business today is much more than financing legal fees; a significant portion of our investments look just to the underlying claim asset value, and legal fee spending is irrelevant. Thus, the relevant addressable market from our perspective is what we believe to be the trillion-dollar or greater annual payment of litigation resolutions.” – Burford Capital 2017 Annual Report

As Burford accurately describes, getting data on total market size or potential is difficult for the legal finance industry. The best numbers I have found suggest current global penetration of litigation funding is somewhere in the low single-digits. However, I believe even that is overstated as the very existence of litigation funding expands the addressable market of legal fees. Getting funding from third parties like Burford allows lawsuits to be tried that previously would not have been filed due to lack of funds. In addition, Burford helps recover assets from lawsuits that were won but never paid by the defendant. That is more market expansion. Suffice to say, I believe Burford is benefitting from a medium-term tailwind from COVID, but I also believe their runway beyond that is long as well.

Historically, Burford has funded 85% of balance sheet deployments with debt, and they just raised $400 million of fresh debt. $50 million of that is going to repay other debt. So, if $350 million of this new debt is used to deploy into lawsuits, and 85% is funded with debt, that would be $411 million in balance sheet deployments. My base case assumes $400 million in 2021.

In an interview from this March, Chris Bogart, when referring to the overall industry, said “there’s absolutely no reason you wouldn’t expect [committed funds] to double in the next five years.” A double in five years is 15% per year. As I discussed above, Chris is not one to exaggerate. So, when I read that quote, I interpret that as him seeing a clear path for a minimum of 15% industry growth for the next five years. Combined with the previous quotes about the demand Burford is seeing, I doubt Chris is expecting his company to grow slower than the overall industry.

Putting all that together, I think Burford’s balance sheet deployments averaging 15% growth for the next ten years is reasonable. If achieved, Burford would be making just under $1.5 billion of balance sheet deployments in 2031. Given Burford’s fast growth in its first twelve years of existence and the demand they are currently facing, I see no reason to think growth is at risk of hitting a wall anytime soon.

Moving onto returns. Looking only at their concluded cases through the end of 2020, Burford has generated 24.9% IRRs. Importantly, Burford makes sure to remind investors on a regular basis that their hurdle rates for new investments have not decreased.

“Broadly, when we originate all these [balance sheet direct] assets, we are targeting risk-adjusted IRRs in the mid-20s to mid-30s with an expected weighted average life between two and five years, though we can, on occasion, accept a lower return on a shorter-lived, more liquid or less risky asset.” – Burford Capital 2020 Annual Report

“We price our capital commensurate with the risks we identify and quantify. Broadly, as we underwrite new legal finance assets, we are targeting risk-adjusted returns consistent with the historic performance of our concluded portfolio, although returns vary widely across different types of investments.” – Burford Capital 2020 Annual Report

Earlier in this post, I discussed how I believe that Burford’s size, reputation, and market share in the high-end of the market will hopefully protect them from becoming commoditized capital. Despite that belief and what Burford says about their hurdle rates remaining the same as they always have been, I still assume in all of my valuation scenarios that IRRs do gradually come down over time. But it is possible I have been too conservative here. Nonetheless, my base case has IRRs going from 22.7% in 2021 to 15.0% in 2031.

Moving on from the core balance sheet operations, the second part of Burford’s business is the funds they manage. As of yearend 2020, Burford manages eight funds with $2.7 billion of outside assets under management (ignoring Burford’s investments in two of the funds). If one were to just look at historical cash generated from these funds, it would be easy to determine this segment is not too important to Burford’s overall financials (dollar amounts below are in thousands).

However, the low level of historical fees generated masks a business segment that should look much better in a few years. Six of Burford’s eight funds have what is called a European waterfall structure. This means Burford does not earn its performance fees until outside investors have made their entire investment back from completed cases. Thus, in terms of the life of a fund, Burford’s performance fees are very backend weighted. I think Burford’s total fees can grow from $24 million in 2020 to $80+ million in 5-6 years because of how these performance fees work.

A big part of this future potential is Burford’s largest fund, BOF-C, that has a $667 million dollar investment from a sovereign wealth fund. Burford’s fees in most of its funds are the typical 2% management fee and 20% of profits, but the sovereign wealth fund pays Burford a flat $7 million per year plus 60% of profits. No, 60% is not a typo. However, this fund was launched in December 2018 and thus Burford is still only making their $7 million management fee.

Going forward, I expect Burford’s fund business to continue to grow and become more profitable. I modeled out each of their current fund structures and I believe that the mature weighted average fees (both management plus performance fees) will be around 1.6% of assets under management. That is what I use in my valuations.

Next, my base case assumes assets under management increase 9% per year from $2.7 billion in 2020 to just under $7 billion in 2031. Given Burford has already announced they expect to raise a new fund this year and four of their last five funds raised have been over $300 million, I expect them to be well ahead of that 9% per year pace by 2022.

“It would be surprising if 2021 did not see us begin to raise incremental private fund capital, although we will continue to balance carefully the advantages of fund capital with the higher profitability of balance sheet investing.” – Burford Capital 2020 Annual Report

Now that I covered Burford’s two segments and what I expect them to generate, let’s move on to operating expenses. Excluding amortization of intangibles from a previous acquisition and fees for listing on the New York Stock Exchange last year, Burford’s total operating expenses in 2020 were $91 million, up from $54 million in 2017.

Looking forward, I expect Burford to benefit from meaningful operating leverage for two main reasons. The first is what I just discussed with respect to their investment funds. Burford has increased the scale of their funds recently (going from $1.7 billion in assets under management in 2017 to $2.7 billion today) without yet seeing the benefits of those performance fees.

“Growth in assets under management over the past several years has driven the current period increases in operating expenses in this segment, while much of the income (in particular, performance fees) would be expected to occur in future periods.” – Burford Capital 2020 Annual Report

Second, their largest asset, the Petersen lawsuit, has required material amounts of spend from Burford. In late 2019, Burford announced they had spent $44 million in operating expenses to date on the Petersen lawsuit, which started in 2015. Given Burford’s total operating expenses from 2015 to 2019 were $281 million, that means the Petersen lawsuit alone accounted for 15.7% of operating expenses in its first four years. Burford did not update Petersen spend for 2020, but some of those expenses certainly continued. However, when the Petersen case is over—as it should be in the next few years—those expenses will go away.

[5/2/21 update: The above comment about Petersen’s $44 million in operating expenses is wrong. I had misinterpreted a comment from management a couple years ago. Those expenses were capitalized, not expensed. Nonetheless, I am leaving this post as originally written for posterity.]

If expenses grow at 11% per year (compared to the balance sheet business at 15% and the funds at 9%), total operating expenses will go from $91 million in 2020 to $288 million in 2031. Next, Burford currently pays very little in taxes, but management has said that mature tax rates will be in the “low teens.” Thus, I assume taxes gradually increase up to 14% by 2031. Finally, I use a 10% discount rate (as I do for all companies) and a 15x terminal multiple in 2031 to represent a healthy but slowing and more mature business at that time. All of that results in a fair value today of $23.15.

To be clear, the future will not turn out as I just described, and I do not think Burford is worth precisely $23.15 today. That high-level walkthrough of my discounted cash flow is just to demonstrate how I think about valuing Burford. Even with what I believe are very rational assumptions given Burford’s strong competitive position in a secularly growing industry, the stock still appears to be quite undervalued. In reality, I have done many versions of the above discounted cash flow using various assumptions and I think a reasonable argument for today’s fair value could be made for anything from $12 per share up to $40. Compared to a current stock price of $10.72, that is substantial upside.

Why this opportunity exists

In late summer 2019, two short reports came out about Burford that sent the shares down around 65%. For that big of a price collapse, one would assume there was hard evidence of fraud, the company was facing imminent bankruptcy, or something to that effect. There was not. Every company I invest in has things to worry about and a legitimate bear case. Burford is no exception. But beyond that type of stuff, I do not think the short reports uncovered anything substantial. In my opinion, it was a lot of innuendos, half-truths, and making a big deal out of things that matter to the long-term value of Burford much less than the reports made them appear.

To me, the most convincing claim was that Burford had misrepresented investments throughout its history. The result of this was returns on invested capital that were overstated. One of the reports walked through four investments that they believed Burford had misrepresented—the most damning of which was an investment Burford made in a case involving Napo Pharmaceuticals.

To speak broadly about Burford, it is important to remember what their core business is: funding lawsuits. Lawsuits are messy, and they last a long time. That is the nature of Burford’s business. Ultimately, Napo is a good example of why I am invested in this company. Burford invested in a complex situation—that became more complex over time—and they were still able to get a decent result with upside optionality attached to it (which did not pan out). However, given the nature of lawsuits, the short report was able to string together a handful of facts and innuendos, and make it appear that Burford completely misrepresented this case to investors.

The truth is that Burford represented the Napo case accurately in the numerous times they discussed it, but explaining it fully required a seven-page walkthrough that spanned eight years of activity (posted publicly in response to the short report). Outside investors cannot expect Burford to provide that level of detail on every complicated case they are involved in. At the time, Burford was invested in over 1,100 claims. Outside of a few large cases, most are simply not meaningful enough to discuss.

Next, partially as a result of these short reports and the resulting share collapse, Burford’s largest outside investor, Woodford Investment Management, closed its doors and liquidated its ~10% position in the fall and winter of 2019.

A few months later, COVID hit, which so far has been a headwind to Burford’s business. In the short-term, some courts are still closed, and lawsuits have been delayed. As I said above, I believe COVID will ultimately be beneficial to Burford’s business, but to date it has not been. Nonetheless, the end result has been kind of a perfect storm of events that have kept a lot of downward pressure on the stock for over a year and a half.

“while COVID has obviously been a global calamity on so many personal and economic levels, the reality of the situation is that lawyers get called into circumstances where there has been disruption and dispute. And the simple fact of the matter is that COVID is going to produce or has already produced a lot of dispute and is going to continue to do that for years to come.” – Chris Bogart, 2020 earnings call

With all that being said, I believe the medium to long-term is very bright for Burford. First, a company can only keep putting up the returns they do for so long without more investors taking notice. And as time goes on, more investors should realize the short reports were not very substantive, the reports will be forgotten, and there will be less career risk for large funds to invest in Burford.

Second, Burford’s results should be taking a step up in the near future. Before 2017, Burford’s annual spend on making new investments was much smaller. In 2016, Burford committed $378 million to new investments. In 2017, that number jumped to $1.4 billion. However, from when Burford first makes a commitment to fund a lawsuit to when they generate a return on that investment averages around two-and-a-half to three years. And given Burford’s investment portfolio did not step up in size until 2017, it would have normally been 2020 when those increased investments started to fully flow through results. However, COVID delayed that.

With the increased scale of Burford’s investments that have not fully flowed through the financial statements, in addition to performance fees for managing their funds that have not yet been earned, I do not think most investors realize how much more cash this business should be generating over the next few years as compared to the last few.

But wait, there’s more!

Finally, Petersen. I purposely waited until the end of this write-up to talk about Burford’s largest asset because I think the company is very undervalued even without it. I also think investors focus way too much on this case. Many investors have made comments suggesting that investing in Burford is a bet on this one lawsuit. I strongly disagree. If Burford’s stock price were $30, Petersen’s value would matter much more to the bull case. At today’s price, it is not very meaningful. If the Petersen case is lost tomorrow, I would happily keep my shares. In reality, I suspect the stock price would way overreact to the downside and I would be loading up on more shares. With that being said, I think Petersen is potentially worth more than the entire current enterprise value of the company, and I believe Burford’s chances of winning are high.

As a quick overview of the Petersen case, YPF is an Argentinian oil and gas company that IPOed on the New York Stock Exchange in 1993. As part of that IPO and to appease concern from potential investors, the Argentinian government guaranteed that if they ever took over control of YPF, they would make a tender offer to YPF shareholders based on a simple and (relatively) objective formula. That was a lie. Argentina took over YPF in 2012 and did not pay out shareholders as promised.

On January 27, 2012, rumors started to swirl about Argentina taking over YPF. Two-and-a-half months later, on April 16, 2012, the Argentinian government announced their intention to take over YPF. Two weeks later, on May 3, the Argentinian parliament made that official. Not surprisingly, YPF’s stock price collapsed during this period from late January to early May. The reason these dates matter is the formula that Argentina promised to pay shareholders from was YPF’s net income per share over the preceding four quarters multiplied by its price/income ratio. And that price/income ratio was quickly declining.

In my opinion, April 16, 2012 makes the most sense to use as the expropriation date as that is the date that Argentina made their public announcement. Using April 16, YPF should have paid out shareholders at an amount that valued the entire company at $18.6 billion.

Prior to the government takeover, a Spanish energy company Repsol owned 57.4% of YPF. Following the takeover, Repsol sued Argentina for roughly 57.4% of that $18.6 billion they believe they were owed, which was $10.5 billion. The two parties eventually settled, and Argentina paid Repsol $5 billion.

Beyond Repsol, two of the other large YPF shareholders in 2012 were Petersen Group, which owned 25.5%, and Eton Park Capital, which owned 3.1%. Burford Capital is now arbitrating these two cases together (which I collectively refer to as Petersen for simplicity). If this case is not settled, and Burford wins based on that $18.6 billion value for YPF, the total winnings would be around $5.3 billion. On that payout, Burford would net around $2.3 billion in cash for itself (Burford’s current enterprise value is $2.7 billion). However, Burford is seeking more than that $5.3 billion by claiming an earlier expropriation date is justified. Argentina is arguing a later date, and thus lower value, is justified.

However, I increasingly do not expect this lawsuit to go through its full trial and appeals process. The following is just speculation by me, but I believe there are several hints that a settlement may be brewing. First, I think it logically makes sense for both parties. The Petersen case started in 2015 and Argentina has successfully delayed and dragged their feet for six years, but the trial is set to start in January of 2022. If this lawsuit goes to its conclusion, Argentina is likely to lose a much larger amount of money than if they settle before the trial starts.

I am not a legal expert, and anything can happen during a trial, but this lawsuit seems fairly simple. Argentina promised YPF shareholders they would pay them if Argentina ever took over the company. Argentina took over the company and did not pay what they agreed to. The opinions from lawyers online and ones I have spoken to have unanimously agreed—calling the case straightforward and regarding Burford as having a high chance of winning. But if that is accurate, why would Burford want to settle for less?

As I discussed above in the valuation section, I think Burford is expecting a multi-year period of high demand for their services, partly due to increased legal activity from COVID. Below is a quote reposted from above about Burford raising a new fund this year, with emphasis added by me.

“It would be surprising if 2021 did not see us begin to raise incremental private fund capital, although we will continue to balance carefully the advantages of fund capital with the higher profitability of balance sheet investing.” – Burford Capital 2020 Annual Report

Maybe the second part of that sentence is just boiler plate language, but it seems like Burford would prefer to match the increased demand they are seeing from balance sheet investments if possible. And what is the easiest way for Burford to get $1-2 billion dollars on their balance sheet? Settle Petersen.

Importantly, Burford has already used this playbook with Petersen before. To date, Burford has sold 38.75% of their interest in the Petersen case to third-party investors for total cash proceeds of $236 million. They did this to help fund their growth the past few years.

“Given the return lags in several of its key business lines, Burford ordinarily would have had only the profits from a much smaller pre-2017 portfolio to fund our growth over the past several years, which would have constrained this growth significantly. That is where the success of Petersen came in. Because we were able to generate significant cash realizations by selling participations in Petersen, we had adequate profitability and funding to build out our infrastructure and invest in the growth that brings us to where we are today.” – Burford Capital 2019 Annual Report

I will not be surprised if Burford uses this same playbook to settle Petersen for good and use those proceeds to fund Burford’s growth the next several years. This is even more conjecture, but I think it is possible settlement talks have already started. On February 18, Burford Capital and Argentina agreed to make all evidence in the trial confidential. These confidentiality agreements are sometimes used when a settlement is being discussed—though not always, and there could be other reasons for sealing documents.

In addition, the Argentinian government has shown more desire to tidy up its debts since Alberto Fernández became president in December 2019. Fernández helped renegotiate a large amount of Argentinian debt last year and it seems they are making progress this year on restructuring the $44 billion they owe the International Monetary Fund. As a former lawyer, I will not be surprised if President Fernández is pushing to settle the Petersen case before it goes to trial and most likely balloons to a much larger liability.

To be clear, Burford settling Petersen this year is not what I am counting on, and it has no bearing on my own personal investment thesis. I have been invested in Burford for years and I hope to still be invested five years from now. Thus, whether the Petersen case is settled this year for less money or won a few years from now for more money should not make a huge difference to the long-term future of Burford, which is what I care about. In addition, my historical track record of predicting catalysts for stocks is abysmal. That is one of many reasons I like owning for the long-term and just being happy whenever catalysts do pop up. Nonetheless, I cannot help but notice a few data points that seem to point to a potential settlement.

Whether the Petersen case is settled or not, it will most likely be worth a lot of money to Burford. Remember, Repsol already settled and got paid from Argentina for a lawsuit that was virtually identical to Petersen’s claims. In addition, Burford has already sold 38.75% of their interest in the Petersen case to third-party investors for $236 million dollars. Sometimes I get the sense that investors think the Petersen case is a 50/50 coinflip and impossible to predict for an outsider. I believe there is plenty of evidence to the contrary.

If the case is settled, I think somewhere between where Repsol settled their case with Argentina at and the low end of the formula I referenced above is a reasonable guess. Halfway between those two numbers would be $3.75 billion in total settlement and $1.68 billion net to Burford. If that $1.68 billion is paid out on December 31st of this year and discounted back at 10%, it would be worth just over $7.00 per share today.

On the other hand, if the Petersen case goes to conclusion and Burford successfully argues for the high end of the formula range, that would be $10 billion in winnings and $4.5 billion net to Burford. In this scenario, the trial and several rounds of appeals will most likely last years. If that $4.5 billion is paid out on December 31, 2025, and discounted back at 10%, it would be worth just over $13.00 per share today.

In reality, there are an infinite number of possibilities here. Petersen could settle for more or less than my example. The trial could start and then be settled midway through. The appeals could go to conclusion and Burford loses. Burford could win more than $4.5 billion and in a shorter timeline than I expect.

Overall, however, I think it is reasonable to expect the Petersen case to be worth between $5 and $15 per share to Burford shareholders today. Adding these Petersen numbers to my above range of fair values for the rest of Burford’s business results in a total fair value range of $17 per share up to $55. Given the current stock price of $10.72, I believe there is a very large disconnect between what Burford is currently being valued at by the stock market and what it will ultimately prove to be worth.