Lemonade is a consumer insurance company that currently offers renter, condo, home, auto, pet, and life insurance. While most insurance companies that consumers are familiar with—Progressive, GEICO, State Farm, Nationwide—were founded 80+ years ago, Lemonade was started in 2015 by the current CEO, Daniel Schreiber, and COO, Shai Wininger.

Not surprisingly given that timeline, Lemonade is a much more tech-oriented company than their larger competitors. Lemonade does not sell its insurance via agents and brokers, instead focusing on online ads, fun social media presences, and word-of-mouth that comes from their high net promoter scores. Lemonade insurance can be purchased in just a couple of minutes from their bot, AI Maya, and one-third of claims are handled entirely by AI Jim—with zero human interaction. This tech advantage is obvious by simply using the product. I have now switched all of my insurance from Progressive and GEICO to Lemonade due to their tech and app being so much better.

This tech advantage is partially due to Lemonade’s commitment to having a single tech platform built from day 1. And this is not something any of their more mature competitors will ever be able to replicate. The legacy insurance companies have tech stacks cobbled together through decades of M&A that cannot be undone.

Geico’s technology needs a lot more work. It has 600 legacy systems that don’t talk to each other. – Ajit Jain, Berkshire Hathaway 2023 annual meeting

Since launching, Lemonade has garnered a lot of positive attention due to their focus on charity. Lemonade is a Certified B Corp, 1% of their common stock goes to the Lemonade Foundation, and a small amount of unpaid premiums each year are donated to charities chosen by their customers. This is a very different image than how most insurance companies are viewed by consumers. As Daniel said, he “wanted to create an insurance company that has an entirely different word cloud associated with it.”

Despite the tech advantage and charitable image, I do not expect Lemonade to put a dent into Progressive or GEICO’s business anytime soon—or maybe ever. But that does not matter. Consumer insurance is not a winner-takes-most market. It is very fragmented, and the best insurers have been successful over many decades. Lemonade succeeding does not require them taking share from the leaders.

Stealing customers from other insurers is difficult because consumers are generally quite sticky to their insurance companies. When was the last time you switched insurers? Overall, it does not happen much because switching is a hassle—especially when consumers tend to bundle multiple lines of insurance with one company. Insurance is also complicated. If your insurance has worked for you, it may feel safer to stick with it as switching could result in minor coverage differences that cause a problem.

Nonetheless, Lemonade’s customer acquisition model is not focused on convincing consumers to switch insurers. Lemonade focuses on getting new customers—young adults buying insurance for the first time—and then keeping them as they become more valuable users of insurance over time.

The first insurance that young adults often buy is renters’ insurance. But relative to home and auto, renters’ insurance is a small and not very valuable part of the consumer insurance industry. That is why many established, traditional insurers do not focus on it. Renters insurance was Lemonade’s wedge into the industry—reminiscent of Netflix licensing “crappy” old shows and movies as a way to wedge into the media industry.

As of late 2022, Lemonade had 9% market share of the entire US renter’s insurance market. From launching in 2015, I think that is pretty impressive, but it actually understates what I care more about. As I said above, insurance is a sticky product and it can be difficult to steal customers from competitors, so I care more about Lemonade’s success with young consumers who are buying insurance for the first time. In 2022, Lemonade had 15% share of first-time renters across the US. Even better, they had 22% market share of first-time renters under 35 years old. That leads the industry. Lemonade’s tech and charity focus have clearly resonated with the younger generations. And those younger customers are growing to become more valuable over time.

[Lemonade is] over indexing on younger and first-time buyers of insurance. As these customers progress through predictable lifecycle events, their insurance needs normally grow to encompass more and higher-value products: renters regularly acquire more property and frequently upgrade to successively larger homes; home buying often coincides with a growing household and a corresponding need for life or pet insurance, and so forth. These progressions can trigger orders-of-magnitude jumps in insurance premiums. – Lemonade S-1

As evidence of this, Lemonade’s premium per customer has grown 20-30% every year since IPO, and I believe their runway for continued and consistent growth is very long. As of Q2 2023, Lemonade earns $360 per year per customer (+24% year-over-year) compared to the industry average for the US at over $3,000 per customer.

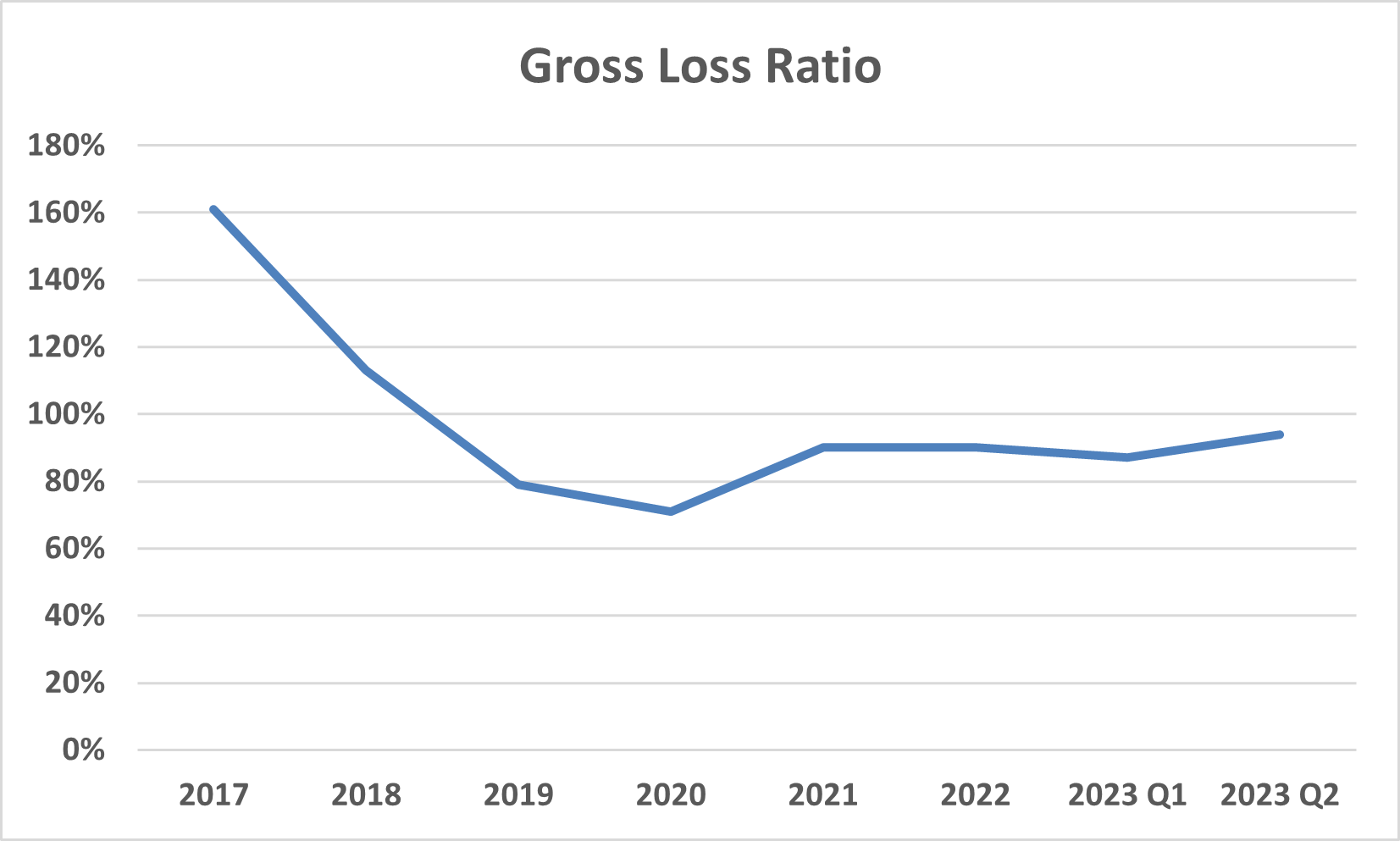

Lemonade’s stereotypical customer is a young adult who buys their first insurance product—renters—from them. Over time, that young adult buys a pet, a car, and a house. If Lemonade keeps them happy and offers bundling incentives, many of those customers that started out spending $150 per year for renters’ insurance will end up spending 10x or more on several lines of insurance. And expanding a customer’s spend like that comes at almost no incremental cost to Lemonade. This land-and-expand nature of insurance is a great feature, but insurance can also be a very tough industry. Look at Lemonade’s historical gross loss ratio.

It is easy to look at that chart and say Lemonade sucks at pricing insurance (as many bears do!). But there is a lot of nuance behind the above chart. The left half of the chart shows that their gross loss ratio decreased from 161% in 2017 to 71% in 2020. That is a very significant improvement. But since 2020, gross loss ratios have been in the high-80s to mid-90s. What changed? A perfect storm of sorts.

From Q3 2020 to Q4 2021, Lemonade launched three new products: pet, life, and auto insurance. New insurance products have high loss ratios in their early years for two reasons. One, a company’s pricing models should get more accurate over time, but they are worse in the beginning when they have the least amount of data. Two, loss ratios are generally highest with new customers and then decrease and flatten out over time. So, when a new insurance product is launched, less accurate pricing is sold to a base of customers that is entirely new. As that customer base naturally ages over time due to new customers accounting for a smaller portion of the overall customer base, loss ratios come down.

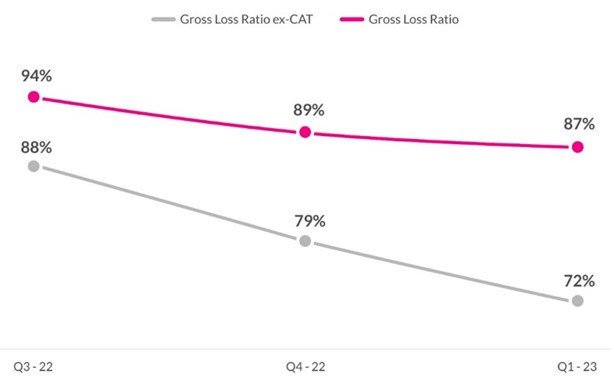

In addition to these three new products being launched, the insurance industry in general has faced numerous catastrophic events lately. Lemonade provided the below chart in their Q1 2023 investor letter.

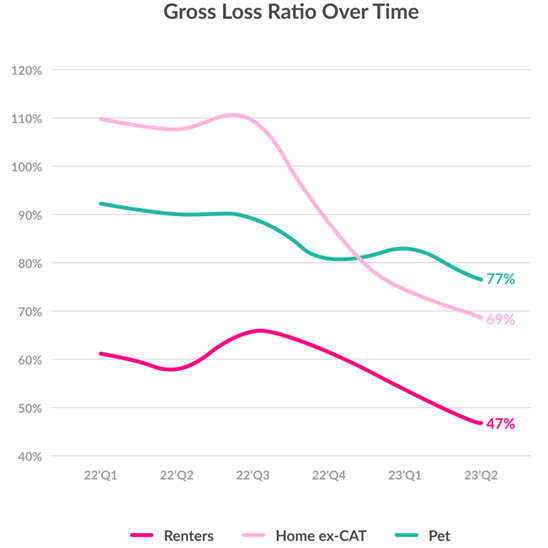

And the below chart from Q2 2023 really emphasizes how much they have been hurt by catastrophic events hitting their home segment as of late (home accounts for most of their recent loss ratio increases).

Now, I am not arguing here that catastrophic events should be ignored. However, it is important to keep in mind what problems are industry-wide vs company-specific. Today, relative to their larger competitors, Lemonade is not very diversified—by types of insurance or by geography. A handful of CAT events over the past few years have meaningfully hurt their gross loss ratios. But how much these types of events impact Lemonade should naturally decrease over time as their new insurance products grow and as they become more geographically diversified.

Finally, interest rate increases are also affecting the entire industry. And adjusting premiums for increased cost is always delayed as state insurance regulators have to approve rate increases. Lemonade recently received significant approvals in California—the largest insurance market—for their home and pet lines, but auto is still pending. This headwind will gradually subside throughout 2024.

While launching three new lines of insurance in the past three years has been a headwind to Lemonade’s loss ratio, it has been a tailwind for customer retention. When customers are able to bundle multiple lines of insurance together, their retention goes up significantly—so it makes sense that Lemonade’s overall retention has steadily increased the past few years. Also, first-year customers generally have the lowest retention, and they become stickier over time. As Lemonade continues to grow and their growth rate naturally slows, new customer cohorts will become a smaller part of their overall business. As mentioned above, this natural aging of Lemonade’s customer base will improve several of their metrics over time.

Finally, renters move more often than condo or homeowners, so renters have lower retention. Lemonade started out only offering renters insurance, and as that becomes less of their business over time, overall retention should naturally improve. Illinois, Lemonade’s first state that offered all of their products, went from 87% annual dollar retention to 95% in one year. I expect Lemonade’s overall annual dollar retention to continue to tick up into the 90s.

Concerns

While there are a lot of things I like about Lemonade, as with any company there are also things I worry about. Today, most of my concerns are related to insurance in general as opposed to Lemonade-specific. Not that there aren’t execution risks of course, but the biggest company specific concerns have mostly gone away in my opinion. At one point, it looked like bankruptcy could be realistic, but that seems very unlikely now. When I first invested a couple of years ago, bears brought up Lemonade’s churn and economies of scale a lot. I think both of these issues are in the rearview mirror or are about to be given Lemonade’s full product offering that should be available in all states sooner rather than later.

The biggest company-specific concern I have is their transition from renters’ insurance, which is not the most competitive line of insurance, to home and auto. In addition to being more competitive, home and auto are also more complex. Lemonade has offered home insurance for years, but they have purposefully kept that segment small. Going forward it will be a bigger part of their business. Likewise, Lemonade has made major investments in building out auto insurance the past couple of years. With inflation increasing this year, auto has had a bit of a delayed start, so success is yet to be determined. With how important bundling is in the insurance industry—both for price discounts and for customer retention—I view Lemonade’s success in home and auto as crucial.

On a very different note, the other Lemonade-specific concern I have is Israel’s conflict with the Hamas terrorist organization. As of yearend 2022, 315 of Lemonade’s 1,367 employees (23%) were based in Tel Aviv, Israel. Frankly, I am the last person who should be commenting or predicting how a conflict in Israel might go, so I’m not going to bother. This conflict could end up being meaningless to Lemonade or it could have a negative effect. Daniel did make some positive comments about the business in his update just a few days ago after the attack. I will say one thing: I was surprised Lemonade’s stock only fell 2% on the Monday after the initial Hamas attack. When even bad news does minimal damage to a stock price, I generally interpret that maximum pessimism is already priced in.

Beyond that, there are several ongoing changes in the world that will have uncertain effects on the insurance industry. With cars becoming more like software every day, consumers need for insurance—especially from third-party insurance companies—may decrease. Lemonade, Progressive, and others offer telematics to drivers in order to better price auto insurance. But Tesla has far more information on their drivers than third-party insurers ever could, so it makes sense that Tesla has started insuring their own customers. Other auto manufacturers may follow suit. Beyond that, autonomous cars and smarter homes could possibly decrease the demand for those lines of insurance over time.

However, my biggest concern with Lemonade—and insurance in general—is climate change. If extreme weather events continue to become more common, it is possible that insurance models as a whole become less predictive. And because there is always a lag with getting proper rates approved by regulators, industrywide models may permanently be behind reality. This would decrease returns on capital in an industry that already does not have the best track record.

However, many of these companies use debt to generate respectable returns on equity. Based on my calculations, Lemonade is already generating good unit economics, and I expect them to have good returns on equity when profitable. But this is far from guaranteed in a tough industry like insurance.

Insurance is mostly seen as a commodity by consumers, so price sensitivity is very high and pricing power by the insurer is very low (and highly regulated). Even worse, it is not uncommon for insurers to purposely underwrite at a loss in order to get more premiums to generate higher investment returns. Finally, capital requirements are regulated, so a lot of an insurer’s capital base is out of their control. The way to generate superior returns in insurance is to either operate the rest of the non-capital cost base with more efficiency (lower cost structure = lower prices) or to attract higher quality customers who cost less. I think Lemonade has a chance at both.

First, as mentioned above, Lemonade became popular among consumers at least partially because of their focus on charity. Especially among younger generations, using an insurance company that focuses on charity as opposed to denying claims (i.e., public perception of most insurers) is an attractive proposition.

When a new Lemonade user signs up, they choose what charity they want their portion of unused premiums to go to. And when that person makes a claim, Lemonade reminds them of the charity they are supporting. I have made a claim with Lemonade, and I thought this part was really well done. It is a subtle—and net positive—way to nudge insurance users to not exaggerate claims or submit false claims, which is a major problem in the industry. If that user gets paid for an exaggerated or false claim, less money goes to the charity that they want to support.

Is it possible that Lemonade’s image as a charitable insurance company attracts a user base that is slightly more honest than the overall pool of insurance users? I think so. In its first several decades, GEICO benefitted from a similar effect as their customer base of government employees was more financially stable and made less claims than non-government insurance consumers.

Second, I believe Lemonade’s technology advantage may lead to more efficiency relative to their competitors. In a commoditized industry where price is crucial, this could be very important. Having a more efficient business means a lower cost structure and thus the ability to offer lower prices.

Today, Lemonade has over 1,400 customers per employee. Public insurers like Progressive and Allstate have a few hundred customers per employee—and generally under 200 if you include agents (which you should). This is not a perfect comparison, and I won’t be surprised if Lemonade’s number comes down over time, but that is too large of a difference to ignore. Frankly, I would be kind of surprised if Lemonade’s single tech platform built in the past eight years couldn’t outperform hundreds of legacy systems cobbled together over many decades.

Can Lemonade’s superior tech and app experience increase customer satisfaction and thus retention? Possibly. I would not switch to GEICO today for 10% savings across my bundled insurance. The Lemonade experience is just too much better. I used the Lemonade app recently to change my policy and I remember being surprised at how delightful of an experience it was. Before Lemonade, I don’t know if I have ever had a delightful interaction with an insurance company or app.

Anyways, yes, I do recognize that I am not representative of most consumers. Most Lemonade users probably would change for a 10% savings. But I also think in a commoditized, price sensitive, low margin industry like insurance, a few small differences at the margins can add up to be meaningful. Focusing on charity and technology might be two of those small differences.

Importantly, I think there is precedent for this in the industry. I have seen many investors say things like “there are already large, successful tech-enabled insurance companies, so Lemonade isn’t doing anything new.” To me, that is the wrong way to look at it. Historically, the most successful insurance companies have led the industry in technology. Today, the best personal insurance companies like Progressive, Allstate, and GEICO are also considered to be the most tech focused. I see Lemonade as simply the next iteration of this trend.

Management

I would not own Lemonade were it not for the two co-founders, Daniel Schreiber and Shai Wininger. They are extremely bright, communicate well, do not over promise, and have allocated capital well.

One of the main ways I judge management is just by consuming their writings and interviews. Are they conservative? Do they understand the underlying drivers of their business? I believe clarity of thought shows itself through clear and concise writing. Lemonade’s S-1 was very well written in simple and easy to understand language. Their quarterly letters are the same. The below quote is a perfect example of this. In simple language, they explain why they are starting to offer term life insurance and the potential rewards, while also being conservative and managing expectations.

Teams we respect at other tech-enabled insurance companies have at times struggled to make the economics of digital acquisition work with term life policies, and we offer no assurances that we will fare any better. We are placing a bet on term life, then, not because we have high conviction it will be a winner, but because its expected value is high: the ante is modest, the odds are fair, and the prize is big. The ante is modest because we will not be underwriting term life policies ourselves, and we will be leveraging the technologies, customers, and brand we’ve already paid for. The odds are fair because the same ‘me to we’ lifecycle events that trigger a graduation from renting to homeownership are often triggers for buying one’s first life insurance policy too. The average age for buying a first home is about 33 in the US, which is also about the average age that college grads have their first child and is also about the average age of Lemonade’s customers. The prize is big because the global term life insurance market stands at about $800 billion this year and is expected to grow more than 10% CAGR to over $2 trillion by the end of the decade. – Lemonade Q3 2020 Shareholder Letter

This conservativeness has shown itself in many ways throughout the company’s life. Even though their gross earned premium has been growing 50%+ for years, they have purposefully tampered down growth pretty much since the company was founded.

Lemonade started receiving inquiries for pet insurance the first week they launched but did not start selling pet insurance until Q3 2020. For years they refused the majority of homeowner insurance requests they received because they did not feel their pricing and algorithms were where they needed to be. Before launching auto insurance, Google Trends showed meaningful interest in a product they did not even offer.

Today, Lemonade is meaningfully slowing down growth as they wait for rate increases to get passed by regulators. Because of this, they expect modest growth in the second half of 2023 and for growth marketing to not be fully turned back on until sometime in 2024 (pending rate increases).

It is easy to quickly look at Lemonade and see an unprofitable, fast-growing tech company and assume management has spent money with no regard over the years. Quite the opposite, I believe they have grown methodically and have actually shown themselves to be good capital allocators. Lemonade is still a couple of years from breakeven, but management has done a good job of raising cash and extending their runway.

In January 2021, Lemonade sold 3.3 million shares of stock for $165 each to raise $545 million dollars. This was almost exactly the stock’s peak. Investors often talk about public companies buying back stock when it is undervalued, but selling stock when it is overvalued can be just as valuable.

In Q3 2022, Lemonade partnered with Chewy to offer pet insurance to their twenty million customers. Instead of paying Chewy in cash for each pet signed up, Chewy is offered one-cent warrants that vest over five years. While giving away equity is not ideal, given Lemonade is not yet profitable and money is no longer free in this economy, I like this agreement. Continuing growth while decreasing the cash cost of acquiring customers has clearly been a focus of theirs as the economy turned.

In June 2023, Lemonade launched Synthetic Agents, which, while poorly named, is basically a structure where 80% of their customer acquisition costs are paid by a third party in exchange for a 16% return over 2-3-years. Lemonade then keeps all lifetime customer economics from then on. For a product like insurance that has long customer lifetimes and such natural routes to increase ARPU over time, I like this structure a lot.

Finally, Metromile was acquired in July 2022 for net cash: $145 million in Lemonade equity against $155 million in cash received. Lemonade also received $100 million of premiums from new auto insurance customers, regulatory approval in many more states than they had at the time (one), and years of driving data that Lemonade did not have, which allowed them to accelerate their own auto insurance ambitions.

With that, I really like how Lemonade treated this acquisition. The Lemonade co-founders have talked many times about how one of their biggest advantages over incumbents is their in-house modern tech stack built on a single code base. Incumbents who have been around for a hundred years and have made dozens of acquisitions simply cannot compare (Adyen has discussed this same advantage of having a single tech stack many times). And that competitive advantage has to be ingrained from day one. However, the Metromile acquisition originally concerned me as a potential step down the wrong path.

But instead of acquiring Metromile and trying to grow that segment immediately, Lemonade did the opposite. They cut off Metromile marketing and let natural churn shrink the business. They did this for several quarters while they fully integrated Metromile into their own system.

We are going to have a single tech stack. We’re determined to do that, which means we have to port everything over [from Metromile]. We’re always going to have a unified single tech stack. – Daniel Schreiber, Q2 2022 earnings call

Lemonade is obsessed with technology because they are obsessed with being a customer centric company. In addition to just them talking about it a lot, it is obvious as a customer myself. Even though I do not need to use my Lemonade app very often, it is a pleasure to use it when I do. It is one of the most well-designed apps I have used, and Lemonade’s focus on user experience is very clear.

In an industry where most of their competitors are disliked by consumers, Lemonade is loved. Their net promoter scores have been in the 60s and 70s since they launched. That is a very high score that is more comparable to beloved consumer software like Apple than it is to an insurance company. An impressive data point was that the net promoter score for Texas residents who filed claims during the February 2021 freeze remained stable. Even more impressive, the net promoter score from customers who have had claims denied has historically been in the 40s and 50s. Users who get denied on the single thing they pay insurance companies for still rate Lemonade highly. That is insane.

Valuation

The quick bullet points here are reaccelerating growth, loss ratios coming down, operating leverage, and a very long runway for growth. Here is what Daniel said recently about growth expectations for the next few years.

Our models now predict that our ‘Minimum Unrestricted Cash’ [in 5-years] would double to >$200m under most scenarios. This holds true when modeling not only for the 12% or 20% CAGR we showed in November, but for growth in the 30s and 40s too. And it’s not only modeled cash that remains pretty constant across growth levels; so too would the timeframe for breakeven. What does change in the models? On a 5-year horizon, those faster growth rates yield severalfold more In Force Premium and Net Income at the end of the period. Therein lies the absolutely transformational potential of Synthetic Agents. The Synthetic Agents go live July 1, and should start doing their cash-maximizing thing right away. For the remainder of 2023, however, we plan to continue to moderate our growth, allowing a few more quarters for our new rates to register on our loss ratio more fully. That done, we will look to ramp up growth, and we anticipate elevated growth rates in the years to come. – Daniel Schreiber, June 29, 2023

So, Daniel is expecting 5-years of elevated growth, previously referenced as being in the 30s and 40s, leading to “severalfold” more in-force premium. In-force premium as of Q2 2023 is $686 million. Severalfold more, in my eyes, would be at least 3x that, or $2+ billion. To exceed $2 billion of in-force premium in 5-years, they will need an average growth rate of at least 25%. I think that is very achievable.

Just growing their premium per customer, as discussed previously, should achieve more than half of that 25% per year growth rate. They have also had very high and consistent growth rates of 50% since going public, so stepping down to 25%+ over the next five years seems reasonable to me. Finally, they are a very small player in the insurance industry.

Lemonade is less than a $1 billion market cap company. Progressive is $77 billion. Allstate is $28 billion. Lemonade has $600 million of gross earned premium over the trailing twelve months vs Progressive and Allstate both over $40 billion. I do not expect the best insurers to go anywhere, but I do think it makes sense that the industry has a true digital-first, modern option. Even Progressive and Allstate, both of which were founded in the 1930s, grew their premiums by 8-10% in 2022. Progressive grew their premiums earned by 20% in 2019, the last year before COVID and the ensuing downturn and inflation. In summary, I believe Lemonade’s runway for 10%+ growth is extremely long.

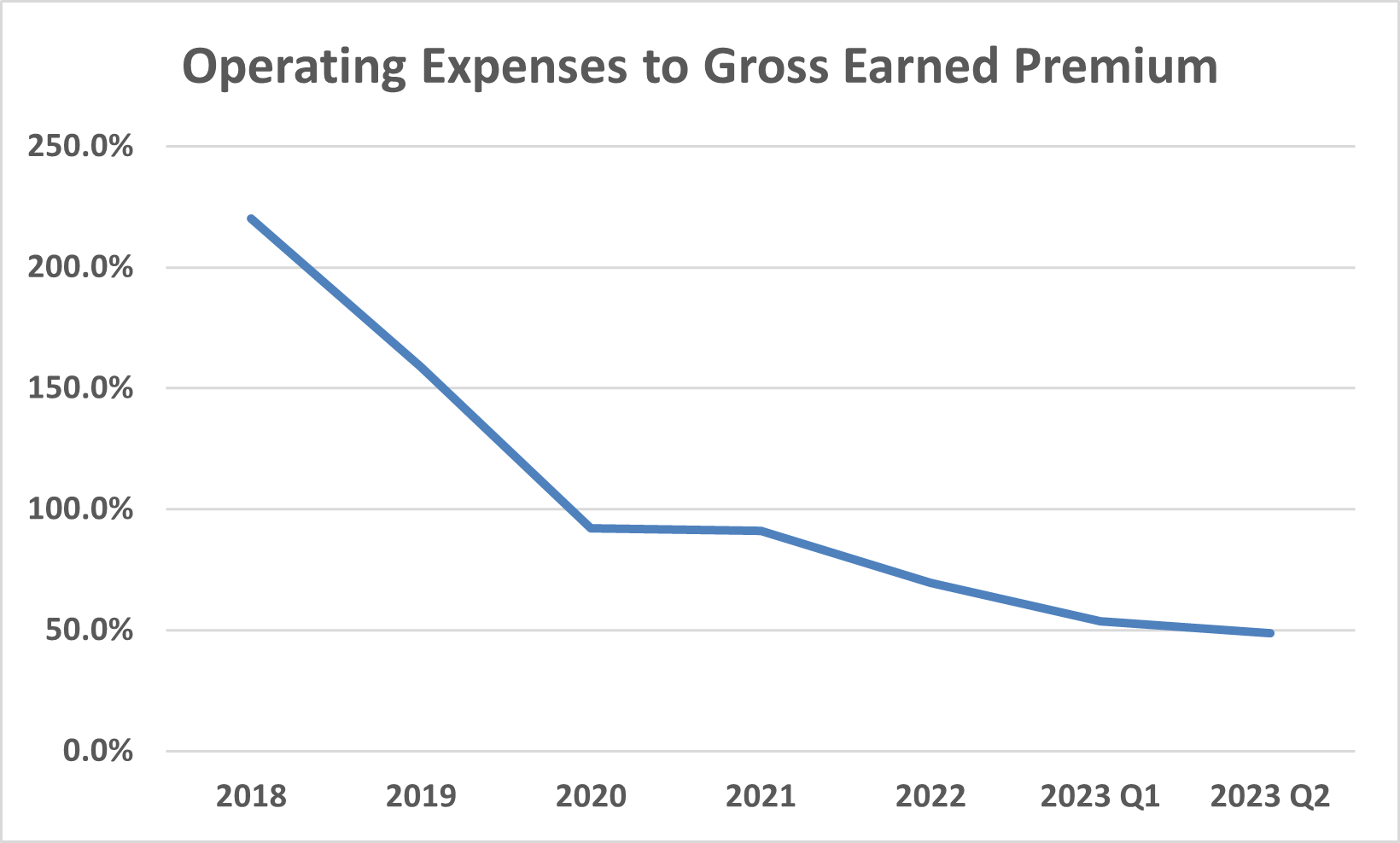

As inflation slows and their rate approvals catch up to the increased cost of living, their loss ratios will come down. As their business grows and diversifies, catastrophic events will impact them less over time. Next, I expect significant operating leverage. One of the key numbers I track for Lemonade is total operating expenses divided by gross earned premium.

As you can see, Lemonade has shown consistent operating leverage over time, and I think much more is coming. I mentioned above that Metromile was acquired in July 2022, but growth was turned off. Lemonade acquired a bunch of employees and then let that new acquisition shrink. Today, growth in their auto segment continues to be muted because rate increases have not been approved yet. Growth overall has been tampered lately due to inflation. This will all change in the next few quarters as rates get approved and growth reaccelerates.

Much of the costlier tech infrastructure building is behind us. And due to that, we slowed our headcount growth significantly… our in-force premium per employee increased by 35% during 2022. Our expenses as a percent of our gross earned premium improved by 22 percentage points during the same period. It’s worth underlining that this progress was not withstanding our acquisition of Metromile, which added considerably to our expense load in the short term. – Shai Wininger, Q4 2022 earnings call

Sum all that up and I think a reasonable 5-year valuation includes 25% per year growth and 5% net margins (though management thinks they can do better). From $605 million of trailing twelve-month gross earned premium, that would come to $1.8 billion of gross earned premium in five years, and $90 million of net income at a 5% margin. A 35x multiple results in a $3.15 billion market cap vs $850 million today. That is 3.7x over 5-years for a 30% IRR.

I am sure many investors will balk at a 35x multiple five years from now, but high multiples are justified for long growth runways. If Lemonade’s growth following the next five years was 15% for five years, 10% for ten years, and then 4% in perpetuity, fair value would be a 38x multiple (at a 10% discount rate). If Lemonade is successful, I think a 35x multiple 5-years from now would actually be conservative. And if Lemonade is less successful, I will not be surprised if they are acquired for more than their current market cap implied value of 1.4x gross earned premium.

Why this opportunity exists

From what I have seen, Lemonade generally gets lumped into either one of two buckets—insurance broadly or insurtech (younger, tech-focused insurance companies). From a high level, Lemonade looks bad in either bucket. However, Lemonade is a much better run company than the other insurtechs. And saying Lemonade is expensive and sucks at underwriting compared to companies like Progressive and GEICO is skipping over a lot of nuance.

Insurtech includes a handful of public insurance companies that were founded relatively recently and have a more tech focus relative to older insurers. Lemonade regularly gets mentioned alongside Hippo and Root. Both of these companies suck. Their strategies are worse, and their management is worse. I would not invest $1 in either of these companies. I have seen multiple times where investors say something about all three companies that is true about Root and Hippo, but not Lemonade.

Similarly, I think a lot of useless statements are made when Lemonade gets compared to insurers like Progressive and GEICO. Those industry leaders have been around for many decades and are mature, slower growing companies. Lemonade is still very young and launching new insurance products requires a lot of upfront capital. Also, insurance companies that use agents expense their customer acquisition costs over time. Lemonade’s customer acquisition costs are all up front, making their financials look even worse in comparison. Going through cash as an insurance startup is to be expected.

Separately, I think because Lemonade is a young, unprofitable insurance company many investors assume the two co-founders have no idea how to run an insurance company and are pursuing growth at all costs. Based on their actions and listening to every conference call and probably close to every interview those two have ever given, that is not the impression I get at all. As discussed above in the management section, I have been very impressed after following the company for over two years.

More specifically as to why this opportunity exists right now, a lot of public tech stocks have been beaten down the past 1.5 years, especially unprofitable tech. Consumer stocks have also been hit lately given the economic uncertainty. For Lemonade specifically, I think Mr. Market is overly focused on near-term headwinds that are going to turn to tailwinds next year.

The most recent quarter, Q2 2023, saw their gross loss ratio spike up to 94% due to more catastrophic events. At the same time, inflation is hurting them as their rate increases are gradually working through the regulatory bodies. Because inflation has hurt their unit economics, they have turned off marketing for certain lines of insurance in certain markets. This is a good thing, but the market never likes slowing growth. Management guided to minimal growth in the second half of 2023 due to inflation headwinds. Growth will be turned back on in 2024 as their rates get approved and unit economics rebound. All of this adds up to a situation that I love: the market is focused on near-term headwinds while ignoring medium-term tailwinds.

As inflation inevitably slows down and Lemonade’s rate increases get approved, their loss ratios should come down. This will also allow them to turn marketing back on and thus growth will accelerate. As their heavy investments to build out their three new lines of insurance are mostly complete, I expect next year’s growth to have high incremental margins and prove once more the operating leverage that Lemonade has. Reaccelerating to 20-30%+ growth while loss ratios decrease and margins increase should result in a meaningful sentiment shift in Lemonade’s stock.

We won’t put pedal to the metal until the loss ratio for new cohorts is in line with our targets across the board. We are already within that range for some of our offerings – Renters and Pet broadly, and Home and Car in certain geos – and this is where our moderate growth will come from. More accelerated growth will wait until more rates come online. We believe we are on the way. Faster rate filings and more approvals bode well, as does slowing inflation. – Lemonade Q2 2023 Shareholder Letter