Shopify is a commerce platform that helps merchants sell across all their sales channels: online, physical retail, social media, and marketplaces such as Amazon and eBay. In 2004, Shopify was founded as an e-commerce platform for new entrepreneurs and small businesses. While that is still a meaningful part of their business, they have moved upmarket via Shopify Plus, which is a higher-end platform that starts at $2,000 per month and manages commerce for brands doing up to around $1 billion in revenue per year.

Tobi Lütke, founder and CEO, has made the comparison that Shopify is like an operating system for retailers. I think this is a good analogy. The platform that runs a merchant’s sales is arguably the most mission-critical system that company has. Like the Windows operating system, once a merchant runs their business on Shopify, they are unlikely to switch to a competitor.

High switching costs have allowed Shopify to run the land-and-expand playbook to a tee: offer a mission-critical product or service that customers struggle to switch away from, and then upsell and cross-sell those users on many other offerings. This increases stickiness, average revenue per user, and customer lifetime value.

The most important tangential offerings they have are a point-of-sale system for physical retail, Shopify Payments to manage the actual transactions, Shopify Capital makes loans to customers to help them grow, Shopify Shipping helps with shipping and returns, and Fulfillment Network is their newest undertaking.

Over the next five years, Shopify is spending around $1 billion dollars to build out a fulfillment network across the US that will manage inventory and logistics for their customers. On the Q2 2019 conference call, Shopify’s COO explained how Fulfillment Network ties in with Shopify Capital and the entire operating system ecosystem.

if we know how much inventory they have… we can make faster, smarter, more intelligent capital decisions. But all these things fit together… We’re beginning to see what we have been talking about [with] this first global retail operating system where merchants come to Shopify and whether it’s housing their inventory, shipping out their products, capital, shipping labels or payment opportunities, we want to do more for these merchants once they come onto the platform and so you are seeing more of that now.

Industry overview

Shopify manages more online stores than any other platform. According to Built With, Shopify currently has 23% market share based on number of websites. The only other competitor with double-digit market share is WooCommerce, which is a WordPress plug-in.

The above chart shows market share for the entire internet. If we zoom in to only the 10,000 largest e-commerce sites, Shopify maintains market share at 21%, but their competitors change quite a bit.

WooCommerce fell from 15% share to 5%. Magento’s share of larger online stores increased. Other than that, the small platforms like Weebly and SquareSpace that were on the first chart were replaced with enterprise platforms such as Salesforce Commerce Cloud and Oracle Commerce. Besides the high-end of the enterprise market, which Built With doesn’t break down, Shopify has the largest market share across all customer segments.

As the above charts show, Shopify has the widest customer base of any e-commerce platform. They have been able to expand from working with the brand-new entrepreneur selling one item up to enterprises doing a billion in sales each year. That is very unique among their competitors.

Wix focuses on the small end of the market. Many platforms, such as WooCommerce and BigCommerce, sell to the small and mid-market segments. Magento, owned by Adobe, concentrates on mid-market and enterprise. Finally, the platforms focusing on the largest online retailers are all segments of the tier 1 enterprise companies: Salesforce, Oracle, IBM, and SAP. Earlier this year, Microsoft announced they are launching an e-commerce store as well.

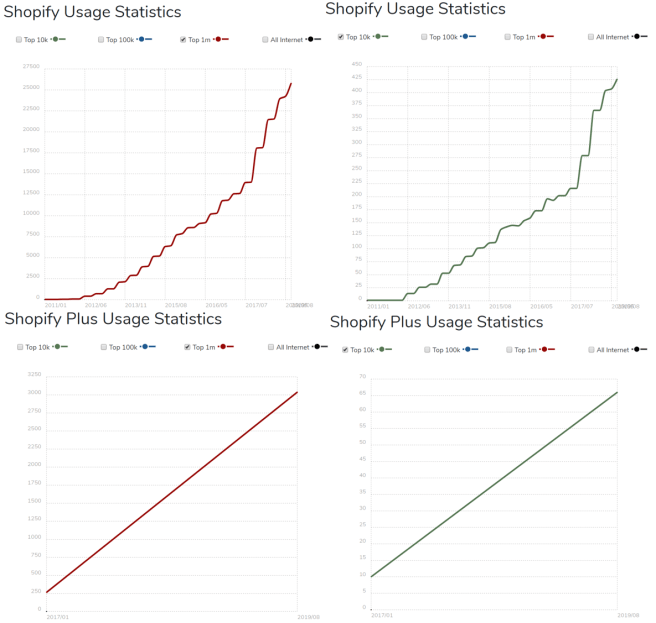

Amazingly, not only does Shopify have the most market share, they are also still growing very fast and gaining more share. Built With allows us to look at individual e-commerce platform usage over time. Below, the top two charts show Shopify usage over time and the bottom two charts show Shopify Plus. The charts on the left show usage among the top 100,000 e-commerce platforms and the charts on the right show usage among the top 10,000 online stores.

Clearly, Shopify is continuing to grow market share no matter how we look at it. Now, I don’t want to post those four charts for all of their competitors, but I have gone through all of them. My main takeaway is that Shopify has the best combination of scale and trajectory in the industry. The only platforms outgrowing them are coming off a much smaller base. Among the platforms that showed the most market share behind Shopify in the first two pie charts—WooCommerce, OpenCart, Magento, and Salesforce—Shopify is growing faster than each of them.

While Shopify has the most market share based on number of online stores, they probably do not have the most share based on gross merchandise volume. That spot most likely belongs to a more enterprise-focused platform like Magento or Salesforce.

It’s also important to remember that most online sales are not done through e-commerce platforms at all. Most is through marketplaces like Amazon and eBay or through stores that are self-managed. While I haven’t been able to nail down an exact statistic, I estimate that platforms manage around 10-20% of all online sales. I believe it is possible that this number increases over time.

E-commerce penetration is still only 10-15% of all retail sales. Thus, there should be many years left of e-commerce outgrowing retail as a whole. And for new brands coming online, using a platform will usually result in faster time to market.

In addition, one of the benefits of Shopify is that they are omnichannel, meaning they integrate all of a retailer’s sales channels into one: web, mobile, physical locations, marketplaces, and social media. As consumers purchase goods from a wider variety of marketplaces and social media sites, retail becomes more complicated. This omnichannel complexity can increase the value of a platform like Shopify that helps manage all of them in one place.

Shopify touts their tangible addressable market as $70 billion. They arrive at this number by multiplying 46 million small and medium merchants around the world by their average revenue per user of $1,500. This calculation was given before Shopify Plus really took off though. So, by adjusting for the number of enterprises worldwide, but also removing countries like China and Russia, I come up with a TAM closer to $20-30 billion.

Shopify’s $1.1 billion in trailing twelve-month revenue is not insignificant compared to my TAM estimate. With that being said, my TAM calculation does not factor in ARPU expansion, which I believe could be significant. I will get into that more below.

“determining our TAM has been a difficult thing for us to do… because every time we turn around there is a brand-new opportunity that presents itself… we think it’s understated.” – Shopify Q4 2017 call

Competitive advantages

Reading reviews and comparisons online for the various e-commerce platforms, it seems nearly unanimous that Shopify is the easiest platform to use and has the largest app store, but their competitors have more out-of-the-box functionality. I think these three things are interrelated and point to Shopify’s competitive advantage.

If I decided to start a new e-commerce platform to compete with Shopify, there’s a lot of functionality I’d have to either build myself or hope to have built via third-party plug-ins. But because my new platform doesn’t yet benefit from scale and network effects, it would be a while before I could expect much of a third-party app store. Thus, I would probably build a lot of the functionality myself. This makes sense. A new e-commerce platform has to offer the necessities that all the established players do.

However, this becomes a problem as that new platform tries to scale because app developers aren’t as incentivized to create apps that compete with the platform’s build-in features. It makes more sense for the developers to focus on platforms where they don’t have to compete with the platform itself.

Shopify’s basic features do enough for most customers most of the time. Because Shopify wants to keep the platform extremely simple and easy to use, they don’t want to add too many basic features. Instead, Shopify has a large app store where merchants can add exactly what they need—and nothing more. This has two major benefits that differentiate Shopify from their competitors.

First, Shopify is widely regarded as the easiest e-commerce platform to use. It seems like their competitors try to compete with Shopify by adding more functionality, but that increases their learning curve and decreases their ease of use.

Second, because Shopify limits their basic features, they need more third-party app developers to fill in that functionality, which kicks in a network effects flywheel. Knowing Shopify has more merchants that could potentially need their apps, more developers are attracted to Shopify as opposed to their competitors. This results in more apps, more competition, and thus better options available for the merchants.

Having the largest app store means Shopify is more likely to have the best functionality because there is more competition than on other e-commerce platforms. Shopify having the most scale means they attract the most third-party developers. Essentially, those developers compete with each other to make Shopify better. This creates strong barriers to scale for Shopify’s smaller competitors attempting to catch up.

These network effects are strengthened by the high switching costs of Shopify users. For a merchant, the platform that runs their online store is very important to their business. Even better, switching costs should increase over time. The longer a merchant uses Shopify, the more familiar their employees become with it and the more disruptive it would be to switch. Mission-critical B2B software that is used by employees on a daily basis to run the business is very hard to rip and replace. And the more successful a merchant becomes, the higher the risk of switching to a competitor.

Being the largest e-commerce platform is now allowing Shopify to do things that smaller players aren’t able to compete with—like spend a billion dollars building out a fulfillment network. Similar to Amazon’s Fulfillment by Amazon, Shopify’s goal is to manage logistics for their merchants. Shipping speed and shipping costs are two of the most important aspects of online shopping.

Via this network, Shopify stores should have faster shipping, lower shipping costs, and thus sell more product than comparable stores running on competitive platforms. This creates a flywheel of Shopify merchants performing better, which leads to Shopify attracting more merchants and funding more logistics build-out. Like Amazon, Shopify’s logistics network should benefit from the aforementioned network effects, in addition to barriers to entry (upfront cost), economies of scale (shipping cost per-unit declines over time), and barriers to scale as a result of all of those combining together.

Shopify’s core business benefits from strong economies of scale as well. Shopify manages payments for around two-thirds of their merchants, which is inherently a service with high operating leverage. Finally, as Shopify merchants grow their own business, fees flow through to Shopify at higher margin.

Risks / bear case

One of the most commonly cited points against Shopify is their high churn. Given I’ve mentioned high switching costs multiple times in this post, how is that possible if they have high churn? It’s important to delineate between the many different types of customers that Shopify has. By numbers, most of their customers—especially new customers—are very small “businesses”—many of them having zero sales. These are individuals testing out selling one or two items, maybe dropshipping from Alibaba, and hoping to get lucky.

A smaller number of their customers, but the majority of their gross merchandise volume, comes from established merchants selling anywhere from low six-figures to a billion dollars’ worth of product per year. I believe these customers, the ones that account for the majority of Shopify’s revenue, have high retention rates. Just thinking high-level, as I’ve stated before, a merchant’s e-commerce website is a very important part of their business. It makes no sense that mission-critical software would have customers churning at a high rate.

I suspect churn is inversely correlated with customer size. Small customers who often have zero sales churn at a very high rate, while established businesses rarely churn. Supporting this, management has noted that Shopify Plus merchants have retention rates in excess of 90%.

Finally, based on my own analysis, Shopify has attractive unit economics, which is what matters the most. The concern with high initial churn is that Shopify will never be able to cut its sales and marketing spend because they constantly have to replace the high numbers of new customers that leave. However, I believe they have attractive unit economics (30%+ IRRs) even if they never are able to decrease customer acquisition costs. The more important inputs are the overall dollar retention rate and getting leverage from G&A and R&D.

“that threshold is $1 GMV. The moment someone sells something, that account is really sticky… we have a lot of effort on trying to just help people get their first sale.” – Shopify Q3 2018 call

Beyond churn, there are a few things that I am more concerned with. To date, Shopify has been very successful in first world countries, primarily the US. In 2018, the US accounted for 70.4% of revenue; Canada, the UK, and Australia combined accounted for 17.5% of revenue; and the rest of the world accounted for 12.1%.

The rest of the world is growing much faster than the overall business though—106.6% in 2017 and 83.1% in 2018. Nonetheless, more of Shopify’s future growth is going to have to come from non-first world countries, which will not be as easy as the past. The below comes from a report that Shopify put out on global e-commerce statistics.

75% want to buy products in their native language. 59% rarely or never buy from English-only websites… 92.2% prefer to shop and purchase in their local currency… Online payment methods weigh heavily on buying decisions… cash on delivery is the number one choice in Eastern Europe, India, Africa, and throughout the Middle East.

Next, Shopify should be more sensitive to the economy than most businesses. If the economy slows down, Shopify would probably be hit by a combination of many of their small and medium customers going out of business, in addition to a decline in retail volume across most of their merchants. All downturns are different, but I expect Shopify’s customer base to be hit disproportionately.

Finally, it seems likely that the next computing platform will be virtual reality and / or augmented reality. Just like Shopify is an internet native retail platform, it is possible that the next computing era could result in new retail platforms that are native to AR and VR. Thankfully, Tobi is well aware of this risk and is already thinking about it. His opinion is that Shopify will democratize access to AR and VR and allow merchants to smoothly make the next technology transition. We’ll see.

Management

Tobi Lütke co-founded Shopify in 2004 as the CTO and is now the CEO and Chairman. Prior to Shopify, Tobi ran an e-commerce company selling snowboards. After experiencing how difficult it was to setup an online store, him and his former partner decided to give up on snowboards and focus on building an e-commerce platform.

Like most founder-led companies, management is well-aligned with outside shareholders. In 2018, Tobi was paid $586k in cash and $8 million in equity. Today, his Shopify stock is worth around $2.5 billion. I really like how Shopify has structured their executive compensation. All executives are paid around $400-600k in salary plus $4+ million in equity that vests over three years. There are no annual cash or equity bonuses.

The CEO Pay Machine is a book I really enjoyed that discusses why most executive compensation is so bad. One of the areas the book zeros in on is annual bonuses. My takeaway was that it’s nearly impossible to have short-term bonuses that don’t have unintended negative consequences when considering long-term value creation. Thus, I like seeing companies like Shopify that subscribe to the notion of reasonable salary + no bonus + vast majority of pay in equity.

Compared to most newer tech IPOs, Shopify also has good corporate governance. Tobi is the CEO and Chairman, and there is a dual share structure. However, Tobi’s Class B shares only give him 33.8% of total votes. While I understand the logic and am invested in companies where the founder / CEO has over 50% control, my preference is for founders to have 20-40% voting share. This gives them significant power and job security, but also inherently has more checks and balances in place.

Similar to executive compensation, director pay is also well thought out. Each board member is paid $50-60k as an annual retainer and then $200k in equity that vests in one year. However, two directors have elected to not receive any pay and one has chosen to take his cash retainer in the form of deferred stock units. Factoring that in, only two directors are paid any cash at all. Besides the director who joined in 2019, the other four outside directors all own meaningful amounts of equity—one is at ~$420k and the others are in the multi-millions.

“Pushing a specific culture sounds weird and dystopian… I want to be different. I want to be myself.” – Tobi Lütke

Finally, Tobi has a lot of interesting views on company culture. As the above quote gets at, he’s kind of anti-company culture as it relates to the popular notion of the phrase. His goal is to hire good people, let them be their authentic selves, create incentives to encourage that, and not bury them under bureaucracy.

Tobi believes one of the main reasons that companies die is executives losing touch with the front lines of the business. Because of this, all Shopify executive hires are required to do customer support when they start. In addition, Tobi still has his own customer support account and takes calls every once in a while.

One of Shopify’s core values is change. Tobi wants to encourage employees to take risks and not be afraid of failure, or as he would call it, “the successful discovery of something that did not work.” If something is undoable, he wants employees to make that decision almost instantly. I got a chuckle out of this tweet a few weeks ago from a Senior Development Manager at Shopify:

“Shopify periodically removes *all* recurring internal meetings from everyone’s calendar.” – Paul Dowman

This is actually one of the recommended ideas in the poorly-named-but-valuable book Double Your Profits in Six Months or Less. As companies get bigger, bureaucracy inevitably sets in—partly because things like recurring meetings get set up and stay in place long after they are valuable. When all recurring meetings and reports are stopped, a significant portion never get restarted. As Jeff Bezos talks about, Day 2 is inevitable at all companies. Putting in effort to delay Day 2 as long as possible is a good sign though.

“Hell would be at the end of my life meeting the best version of myself that I could have been.” – Tobi Lütke

Tobi comes off as a leader who is intellectually honest and obsessed with learning. In multiple interviews, he’s talked about the influence that Daniel Kahneman and systems thinking have had on him. I appreciate CEOs who admit mistakes and play down their success, as opposed to always being positive and promotional. To me, Tobi comes off as more Mark Leonard than Marc Benioff.

“Even now that you talk about [me being a billionaire], it sounds crazy to me. I try not to talk about it… I remind myself how much of this was luck… Why am I the person who ended up winning the lottery five times in a row? I don’t know.” – Tobi Lütke