Spotify has the most global market share of any music streaming service. In 2018, Spotify accounted for roughly 70% of global streaming revenue and 33% of all recorded music industry revenue. Given there are only two other sizable music streaming services, this is a hint that there are large barriers to entry in this industry.

The only three companies with meaningful market share are Spotify, Apple and Amazon: one dedicated streaming service founded in 2006 and two tech giants. Spotify has the benefit of brand name, reputation, network effects, and being synonymous with online music. Apple and Amazon have the benefit of hundreds of millions of users they can cross-sell music to. It would be much more difficult to start a dedicated streaming service today now that Spotify already exists and has scaled globally to over 200 million users.

Spotify’s scale also benefits from their moderately sticky customer base. When it comes to customer captivity, habit is the most bullish datapoint. In 2018, the average Spotify user spent 49 minutes on the platform per day, while premium users spent 80 minutes per day. There was also some evidence that these numbers are increasing over time. Humans are creatures of habit. Having a platform that users spend that much time on everyday is a powerful benefit.

On the other hand, users only experience modest switching costs. Most of this comes from Spotify learning a user’s music taste over time. Thus, a user’s experience should be personalized and improve over time. Anecdotally, I’ve experienced this myself as a Spotify user. Switching to a competitive product would send me back to square one of a service that doesn’t know my taste in music.

Despite that, Spotify’s churn is around 50% per year. From this simple fact alone, their users can’t be that captive. Though to be fair, their churn has decreased significantly over the years, and this should continue into the future. Churn from a specific year’s cohort decreases over time. As cohorts get older, Spotify’s churn decreases naturally. Next, Spotify’s new subscriber retention has increased over time, meaning new cohorts have lower churn than past cohorts.

Finally, a significant portion of new subscribers are rejoins (i.e. ex-subscribers who are re-subscribing). Thus, as the population of former subscribers increases, rejoins should increase on an absolute basis. While I don’t believe Spotify has clarified this, I would guess that rejoins have a lower churn than new subscribers. Rejoins liked Spotify enough to return and they didn’t like whatever alternative they tried.

Another datapoint that I believe supports Spotify not having highly captive customers is that Spotify hasn’t demonstrated having pricing power. Just to keep up with inflation, a $9.99 Spotify subscription from 2009 should cost $11.93 today. Having a subscription service that is essentially getting cheaper over time combined with a variable cost business is not a great combination. With that being said, Spotify did push through a price increase in Norway in Q2 2018, and it seemed to go well. Growth reverted to historic levels and churn didn’t increase.

Finally, Spotify should benefit from numerous network effects. There is more of a social element to Spotify than many other music services. My girlfriend and I are able to easily share music with each other and collaborate on playlists. While not as strong as the network effects that Facebook or eBay have benefited from, this does create a direct flywheel among users wanting their friends to be on Spotify. With that being said, I would rank Spotify’s indirect network affects as stronger.

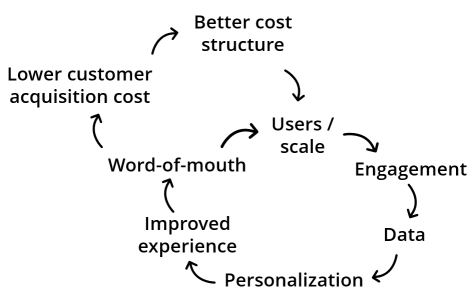

Spotify has the most scale and the most users of any music streaming service. This results in a lot of engagement on the platform and data back to Spotify. Thanks to this data, Spotify is able to continually create a better and more personalized experience for its users. Having a better experience results in word-of-mouth marketing and thus more users and scale.

Industry tailwinds

While the above discussion is mostly focused on Spotify’s current competitive positioning, I believe the major trends of the industry should improve Spotify’s future. First, the future will have more connected devices. The more connected devices there are, the less likely it is that users are completely tied into one ecosystem. Fewer people tied into one ecosystem means more people who want a music streaming service that is device agnostic and works everywhere. That is Spotify. Even better, this should improve the economics of Spotify’s business. Right now, users who run Spotify on more than one device have lower churn and higher lifetime values than users on one device.

Next, music is becoming more globalized. American music has spread to all corners of the globe, but more surprisingly, Americans are listening to music from all over the world as well. With the most global scale, Spotify should be able to take advantage of this trend the most.

“Many predicted the globalized world of streaming would see Anglo repertoire flood other markets. But while international opportunities for Anglo artists have increased, we’re also seeing a huge flow of music back the other way… These international success stories contribute to a virtuous circle which leads to the emergence of even more local artists” – Global Music Report 2019

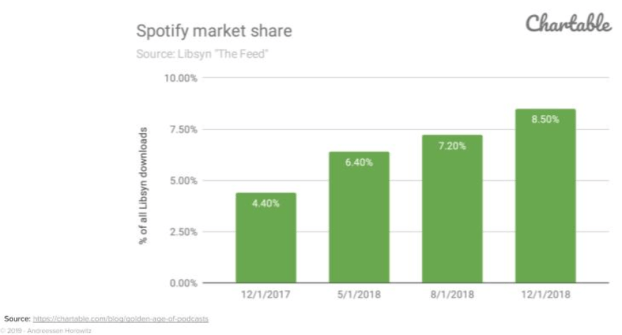

Finally, podcasting is a relatively nascent industry that is booming. As the #2 podcast player in the world, Spotify should benefit greatly from this trend. While Apple continues to dominate podcasting, their share has quickly fallen from 80% to 63% the past few years. Meanwhile, Spotify has been gaining share every year.

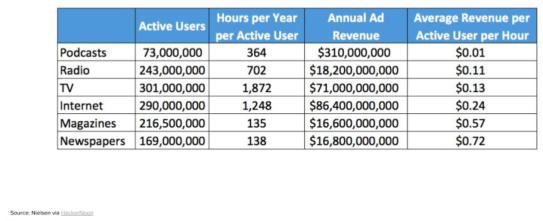

So, podcasting has exploded in popularity and Spotify has been consistently growing its market share. That’s fantastic, but from an investor’s standpoint, what’s even more exciting is that podcasting is extremely under-monetized. The below chart shows how podcast monetization compares to other mediums, the most apt comparison being radio. Podcasts currently monetize around 10x less than radio! I think it’s inevitable that this gap will narrow over time.

Similar to the trend of connected devices, podcasting growth should continue to improve the economics of Spotify customers.

“Podcast content increases engagement through discovery, which leads to lower subscriber acquisition cost, lower churn and then higher lifetime value.” – Spotify Q1 2019 call

Bear case

Around 85% of Spotify’s content is controlled by the three big record labels, plus MERLIN (a digital rights agency that represents thousands of independent labels). It’s great when a company has captive customers that results in pricing power. It’s not great when a company is a captive customer of their suppliers and thus has less control over their costs. With that being said, Spotify has a lot of power over the record labels as well.

In 2001, physical CD and record sales accounted for over 97% of the global recorded music industry revenue. Today, CD sales are down to 25% of the industry. For many years, there was nothing to replace those lost dollars and the industry suffered around 15 years of revenue declines—until streaming returned the industry to growth.

In 2018, streaming accounted for 47% of global recorded music revenue—and Spotify has almost 70% market share of global streaming revenue. Look at the below chart showing industry revenues over time (purple is streaming revenue). If the major record labels want to continue enjoying the growth they’ve experienced the past few years, they have to work with Spotify.

In addition, I believe the labels have to be careful with how much hardball they play with Spotify. The next two biggest streaming providers are Apple and Amazon (followed by Google). If the labels stifle Spotify’s growth, they could end up with a much worse industry structure dominated by tech giants. My guess is the labels actually prefer Spotify as the leader, which bodes well for Spotify’s negotiating power going forward.

Finally, Spotify works directly with many musicians through their Spotify for Artists platform. The more artists that work directly with Spotify, as opposed to using their label as a middleman, the less negotiating power those labels have with Spotify.

All of this has resulted in labels being put in a very tough situation. Spotify is the most popular streaming service and it has the most global scale. Because of this, labels are forced to prioritize Spotify as a promotional tool, or their musicians won’t reach the maximum audience. However, by doing this the labels are making Spotify stronger and reinforcing Spotify as a cultural platform. And if any of the three major labels removes their content from Spotify, that would immediately make the other two labels—their biggest competitors—more valuable.

Management

When I’m studying a management team, two of the main things I’m trying to decipher are 1) are they independent thinkers, and 2) do they understand their business at a deep level? Unfortunately, it’s rare that I answer yes to both of those questions, but I do believe the Spotify team fits the mold.

Are they independent thinkers?

I want to invest in CEOs who think for themselves and aren’t afraid to go against the crowd. This isn’t being a contrarian—it’s just coming to conclusions for oneself, whether others are doing it or not. I believe running a successful business for many years requires the ability to do things differently and risk looking like an idiot. With Spotify, there are some small signs of independent thinking: a direct listing instead of a traditional IPO and quarterly calls that are Q&A only (how all quarterly calls should be!). In addition, I really like their approach to compensation.

Any management team is a win in my book if they don’t default to hiring a compensation consultant, paying salaries in the 50-75% range of some handpicked “peer” group, paying annual cash bonuses based on some combination of short-term financial goals and completely worthless subjective goals, and offering long-term stock options to “align” executives with outside shareholders. Spotify does much better than that.

To their executives, Spotify pays low salaries, no annual bonus, and grants large amounts of restricted stock that vests over five years. Directors receive no cash at all and are paid $300,000 in restricted stock units that vests over four years.

“we incentivize our executive leadership heavily through share-based compensation, which we believe fosters the long-term growth of the company… We have opted not to offer annual cash bonuses to our executive leadership team, as we believe they do not incentivize the long-term growth of the company” — Spotify 2018 20F

Do they understand their business at a deep level?

In my experience, the majority of management teams don’t really understand what drives the underlying economics of their business. Not Spotify. It helps that Barry McCarthy, their CFO, was previously the CFO of Netflix. While I think the analogies between the two companies are sometimes overstated, it does seem that Barry is bringing over some of the Netflix playbook.

Two knocks against Spotify are that they are primarily a variable cost business (which means less operating leverage as they scale) and how much power the major labels potentially have over them. I believe Spotify is doing a good job of addressing both these issues.

First, they are trying to transition to a business model that has more fixed costs via podcasting. Producing original podcasts is a fixed cost but it is also unique content that people must subscribe to Spotify to access. Podcasts have also improved the underlying economics of the business.

“What we see very clearly as we’re investing in more podcast content is engagement goes up, as engagement goes up we both broaden the appeal to new users, but we also increase the engagements of the existing ones on the platform, which drives down churn which in turn makes the business overall much stronger.” — Spotify Q4 2018 call

Next, Spotify is trying to create a two-sided marketplace where both users and musicians are purchasing services and getting value directly from Spotify. If Spotify is able to increase their direct relationships with musicians, labels will continue to have less power.

In addition to podcasts and Spotify for Artists, Spotify is different than several of their top competitors in that they offer both a free, ad-supported version and a paid, ad-free version. The genius behind the free service is that it acts as a customer acquisition funnel for the premium service. And this is a low cost customer acquisition channel because it also brings in revenue via ads.

“Our ad-supported service serves as a funnel, driving more than 60% of our total gross added premium subscribers since we began tracking this data in February 2014… 50% of [monthly active users] became premium subscribers within 36 months on average” — Spotify 2018 20F

Unit economics

One reason I always calculate the unit economics of a company is that it can clue me into how well management understands their business. Spotify is a perfect example.

While estimating the IRR of a new customer is not an exact science, I estimate Spotify is earning around a 30-40% return on each premium user they acquire. After I build that base unit economics model, I start to adjust all the inputs to see how they affect the output. The inputs that have the highest amount of leverage when calculating unit economics are the key performance indicators that I focus on. For Spotify, some inputs, like average revenue per user, don’t change the output as much as I expected. On the other hand, retention is the single biggest lever on the output.

When I first started researching Spotify, I didn’t like how they were doing so many things that decreased their average revenue per user: student plans, family plans, extended trials, and the Hulu partnership. My instinct was that Spotify must be struggling to attract users, so they are forced to offer discounts through all these cheaper options.

Looking at their unit economics changed my opinion. Now, I can see that this is the smart decision. These discounted plans and partnerships are lower priced, but they also increase retention. And lower churn increases the return of a new customer more than less revenue per user decreases it.

And as I mentioned above, management is focusing on podcasts for similar reasons: it increases engagement and decreases churn. Thus, looking at the unit economics of Spotify has shown me that a) retention matters more than anything else, and b) management is focused on the correct key performance indicator, as opposed to focusing too much on average revenue per user.