I’m betting Sitestar (SYTE, $0.0465) is a familiar name to those of you who follow the microcap space. For those who don’t recognize it, I’ll do a quick catch-up. Sitestar started getting attention in 2011 when Jeff Moore (aka Ragnar Is A Pirate) began writing about them and continued updating readers up until June 2014 when he started some activism. If what I write piques your interest, I highly recommend reading through his many posts for an educational and entertaining look at his past 4.5 years of involvement in this company.

What they do

Sitestar doubles as a dial-up Internet Service Provider (ISP) and real estate investor. Bizarre combination but whatever. The former CEO, Frank Erhartic, was an experienced real estate investor and started to use Sitestar’s extra cash flow from the ISPs to buy local properties, mostly foreclosed homes picked up for under $100k. Today, this real estate makes up the vast majority of the company’s value as the ISP is declining 3-5% per quarter. As Jeff got more involved with the company (eventually getting a seat on the board), it became clear that management was not doing its job as stewards of a public company. Long story short, Jeff got together with a couple other investors and eventually fired the CEO in December 2015. Steven Kiel, Portfolio Manager of Arquitos Capital Management, is now Interim CEO. His shareholder letter (linked in the previous sentence) basically says he needs some time to figure shit out and will notify shareholders when there is a game plan (that was my interpretation at least). So what is a dial-up Internet and a bunch of homes in central Virginia worth?

Valuation

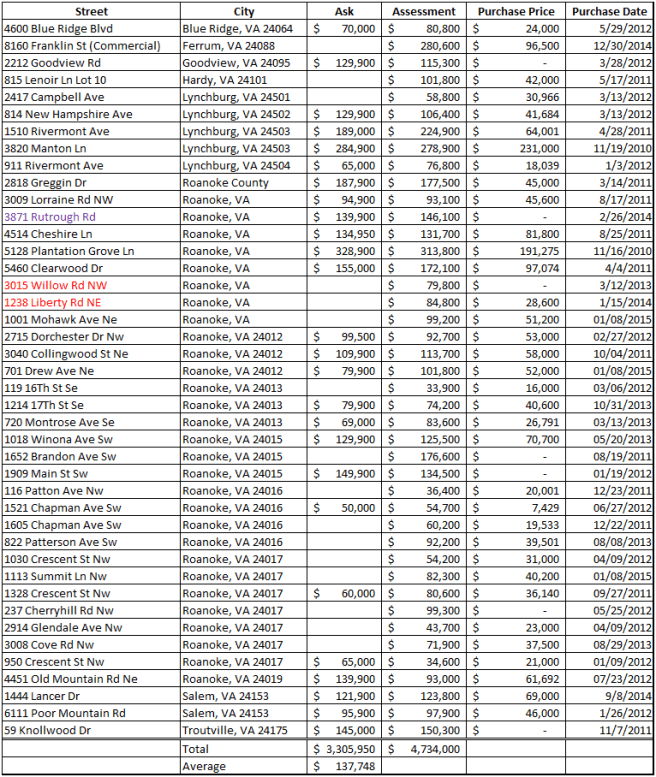

I’ve spent the better part of this week combing through county and city records around the Roanoke, Virginia area trying to find everything Sitestar owns. Their 2014 10-K states “Sitestar currently owns approximately forty-five residential properties” and I’ve found 42, so I’m pretty damn close. Below is a list of all 42.

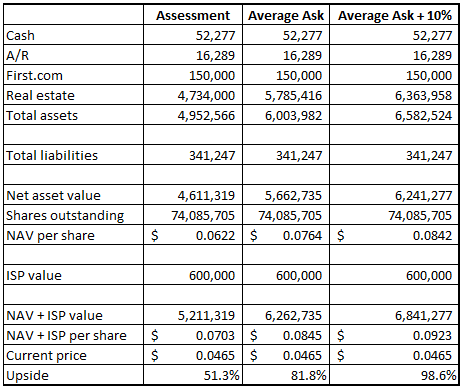

In addition to valuing the real estate, the ISP is worth something. It seems to be cash flowing around $75k per quarter right now. I don’t really know what to value this at, but 2x current cash flow seems reasonable for something low quality and declining as fast as it is. This would value the ISPs at $600k.

They also own the domain first.com which isn’t easy to value either. I tried to find some domain sales that are somewhat similar to first.com—either a low number or a single, short, common word. Below are some of the notable ones I looked at:

- First.de sold for $40,600 in January 2003

- One.es sold for $128,947 in November 2007

- Third.net sold for $475 in June 2007

- Second.lol is currently listed for $29,000

- First.deals is currently listed for $20,000

- Scores.com sold for $1.18 million in June 2007

- Boating.com sold for $250,000 in January 2010

- Camp.com sold for $150,000 in October 2006

- Refresh.com sold for $115,000 in February 2007

- Actual.com sold for $18,000 in April 2012

- Stop.com sold for $62,500 in January 2004

What I gathered from that process is I have no fucking idea what first.com is worth. Next, I went to some websites that attempt to value domains and I received answers ranging from $20,000 to $375,000. Not much more helpful. The thing is, if someone told me it’s fair market value is $100,000 and someone else told me $1,000,000, I’d say both sound reasonable. I used $150,000 in my valuation. Let’s get on with it.

In the below chart, I valued the real estate three different ways. First, the Assessment column is based on the city or county’s most recently assessed value for each property. Assessments aren’t perfect, but averaged over 42 properties it’s probably not bad. The next column, Average Ask, takes the average asking price of the ones that I found listed for sale at some point. In total, 27 of the 42 I was able to find a previously listed asking price for. I then took that average ($137,748) and multiplied it by 42. If you’re skeptical, I don’t blame you. But these properties are pretty damn homogenous—almost all are smaller, single family residences in the same geographic area. I think extrapolating that average to all 42 properties is fine. The thing about the asking prices is that most were listed several years ago, some as far back as 2011. The far right column adds 10% to the previous column’s real estate value to account for several years of a healthy economy chugging along, in addition to the likelihood that I’ve missed one or two properties in my searches.

I think Sitestar is clearly undervalued and it’s now being run by a money manager whose interest is the same as us little guys. So what’s not to like? Well, a lot.

Bear case

I don’t know if this is a bear case, or just questions I have and things that make me squeam a little. In no particular order:

- I’m not positive they are the sole owners of each of the above properties. Sitestar is listed as the owner (except in three cases described next sentence), but they’ve co-owned properties with other entities in the past. The three properties in red and purple on the property list are under separate entities that have Sitestar’s headquarters as their mailing address so I suspect they’re involved. Very possible these are partnerships with other investors. On the flip side, I have probably missed a couple properties they have ownership in because of different companies or subsidiaries being used. It was kind of a fluke I discovered Freedom Virginia Land Trust for example; good chance there are others.

- The ex-CEO’s ex-wife owns Sitestar’s headquarters. Not exactly the person I want as my landlord. And in Jeff’s own words from a 2012 blog post: “Moving the HQ would be a nightmare (after going in and seeing all the wires going all over the place), I couldn’t imagine how much it would cost… plus the service disruption!?”

- Frank and his ex-wife are listed as jointly owning 33% of outstanding shares as of March 30, 2015. This is odd because I’d think these would get split up in the divorce, though maybe it wasn’t final yet. I was calling around to local court houses trying to find their public divorce records Friday afternoon, but unfortunately the courts closed before I succeeded. Either way, these two individuals who were just kicked out of their company still have a significant say in shareholder votes.

- There is also a long way to go to improve their corporate governance and financial reporting. Historically, their filings have been comically bad. My favorite is the 2013 10-K that lists Jeff Moore’s age as 50 (he was in his late 20s at the time). In general though, there have been lots of typos, numbers that don’t add up, and just sloppy stuff all around. I have little doubt Steven Kiel will get this part righted, but I wouldn’t be surprised if previous reports have to be restated in the process.

Conclusion

One thing I’ve been pondering a lot the past few days is “what’s the end game?” The ISP business won’t be around much longer. Does Sitestar evolve into a real estate developer for Central Virginia? Seems unlikely. Put the ISP into run-off mode and liquidate the properties over the next few years? Doesn’t sound terrible.

I’m busy the next couple weeks, but I’m hoping to take a trip to Roanoke after that and do some in-person scuttlebutt. One question I’d like answered is what kind of condition these houses are in. Some have been rentals, but I get the impression quite a few were bought out of foreclosure and have been sitting around collecting dust. Only four are currently listed for sale.

In conclusion, I haven’t decided on this one yet. I look forward to hearing Steven’s next update and the progress he’s making.

Hey Travis,

Great research! One question:

I noticed you didn’t record the ‘notes payable’ of $ 900K as a liability. As I’m not that experienced in accounting, could you explain this?

LikeLike

Nevermind, I overlooked it was in litigation and has been settled for $ 90k 🙂

LikeLike

Interesting analysis…I had owned SYTE in the past, and sold out for a small profit.

Three things I would add…

Previous management was strictly amateur hour. The condition of some, most, or all of the properties may be “lacking”. Also, note that the asking price for most properties is BELOW the assessed tax value. This further indicates that the properties may be in poor condition.

I have known Jeff Moore for years. He is a skilled businessman with quite a bit of experience in real estate and real estate rehab. If he is involved, I am sure that he will do a very good job getting the properties rehabbed.

Finally, if previous management decides to sell, this could put tremendous pressure on the share price. Also, if the USA market slides back into recession/depression that could also put pressure on the share price. Of course, this may provide a buying opportunity.

LikeLike

Your last paragraph is a good point. The previous owners aren’t exactly Wall Street investors so them attempting to dump 33% of shares could be interesting. I’m sure that’s one of the many things Steven and Jeff are discussing. Might be worth it to raise some debt and buy them out at a small premium. And your first point is exactly why I want to see properties in person.

LikeLike

Hey Travis, you might want to take a look at the building 601 salem ave, roanoke va. The owner is listed as (601 salem avenue land trust) which is where we stored everything in the basement under City Dogs one of the two renters. Frank would charge sitestar 600 a month for storage. Feel free to contact me worked for frank 2012-2015

LikeLike

Thanks ace, hadn’t come across that 601 Salem Avenue Land Trust before. That entity also own 2745 Beverly Blvd which appears to be a residence. And I’m betting $600/mo for Sitestar to rent out some basement storage wasn’t exactly fair market value.

LikeLike

Ali of the properties are in disarray.

LikeLike

If you believe a liquidation makes sense and are valuing the company on that basis, don’t you need to subtract the salaries the company will pay and other expenses it will incur during the liquidation period?

LikeLike

I’m not sure what the best route forward is, but liquidation is one of the options. It’s possible there’s a lot of real estate opportunity in Virginia for example. If a liquidation does happen, then yes some SG&A needs to be capitalized and subtracted from the valuation. I imagine they could liquidate this with only a couple of employees though.

LikeLike

I did this same analysis a month or two ago, maybe we can synch up the property listings. I also added the Zillow estimates to each property as a gauge for valuation.

I have also heard that the condition of the properties is not 100%, so expenses would be needed to bring the properties up to par, but I have not been able to get feet on the ground to search out my list of properties. I’d be very interested in hearing about your trip to roanake/lynchburg if you do make the trip.

Since the management shakeup, I’m much more pleased with the possible direction of the company and possible realization of the value of the real estate. The large ownership position of Frank could be a problem, but there may be some hope on that front. Waiting to hear the official updates to come from Kiel and company.

LikeLike

Absolutely. Did you find any properties that weren’t on my list?

LikeLike

You had one that I didn’t have on my list (1238 liberty), and we matched 41. I have 5 properties on my list and I believe they are the ones in Bedford county. I had a hard time getting exact addresses on some of the Bedford county properties, but have some of the assessed information and building type etc…

LikeLike

My name is Greg Holdren , me & my lady Faye king worked for frank the last 2 1/2 years refabing your houses call me at 540-293-1823 for any info on any properties or the way things were handled

LikeLike

things have changed dramatically…

LikeLike