I’ve been looking at several SaaS (software-as-a-service) companies as of late. In laymen’s terms, SaaS is software that is hosted by the providing company and the customer pays a regular subscription fee to use it (as opposed to purchasing the software up front for a one-time fee and hosting the software themselves). If you were to write down a list of characteristics you seek in investments, I bet the typical SaaS company checks off most items on your list. GlobalSCAPE Inc (GSB, $4.10) is one such company that possesses the following:

- 95% gross margins

- Free cash flow margins around 15%

- Over 100% returns on capital

- Over 50% of revenue is recurring

- Good visibility into future revenue

- Little to no customer concentration (no one over 10% of revenues)

SaaS also lends itself to all of the best competitive advantages: network effects, pricing power, switching costs and recession resistant (specifically the last two in GSB’s case). GlobalSCAPE sells enterprise file transfer solutions. If you’ve ever needed to email a very large file or upload one using FTP, you may have noticed some inherent limitations to the standard free (or cheap) offerings. Large enterprises pay companies like GlobalSCAPE to handle these file transfers for them in a much more robust, and most importantly secure, fashion. A lot of GlobalSCAPE’s legacy clients host the software themselves, but the majority of new clients are under the SaaS model (they pay GlobalSCAPE to do the hosting). Combining SaaS revenues with their annual maintenance and support contracts creates a lot of recurring revenue that should slowly creep up (as a percentage of revenue) as time goes on. Recurring revenue was 56% of sales in 2014.

High switching costs are inherent in SaaS providers because the software is usually a crucial part of their client’s business. Think about Microsoft Excel and how much effort it would take a corporation to switch every employee over from using Excel (which they have all been using and are comfortable with) to a competitor product (if a real option even exists, it’s basically a monopoly). While not as extreme, this situation is similar to GlobalSCAPE’s offering. Once a client chooses GlobalSCAPE as their file transfer provider, they will spend significant time getting employees up to speed on using GlobalSCAPE’s software. If they use this software for two years and a competitor comes in with a similar product at a 10% lower price, is it really worth the effort to switch? In most cases, no. Keeping software consistent so all employees are comfortable with it adds more efficiency to the organization than what would be gained by switching software providers. Switching would create months of headaches and decreased efficiency as employees learn the new software. This is why GLOBALscape’s renewal rates are over 90% (they don’t get any more granular than that). As great as switching costs are, the flip side is your competitors have the same benefit. In a mature industry (I don’t think the managed file transfer industry is there yet) with high switching costs, getting new clients is just as hard as losing current ones.

Companies selling products that have high switching costs are also going to be more recession resistant for much of the same reasons. In most cases, it’s simply not worth the headaches to switch to a slightly cheaper competitor to save some money during a downturn. The cost savings or feature differences have to be very significant to make up for the cost of switching.

Valuation

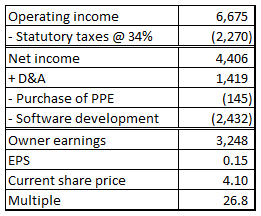

Another nice benefit of the SaaS business model is there’s usually good visibility into future sales via deferred revenue (maintenance and support fees already collected but not yet realized on the income statement). It’s easy to look at GlobalSCAPE’s deferred revenue and feel comfortable their growth will continue (at least in the near-term). Unfortunately, I am far from the first person to realize the benefits of SaaS business models and the valuations in these companies usually reflect that. Below is my calculation for GlobalSCAPE’s normalized owner earnings over the past 12 months (in thousands).

27x for a growing, high quality business seems pretty reasonable, but it’s hardly what I’d call egregiously cheap. To me, GlobalSCAPE is in the realm of fair valuation right now. My preference for a company like this is to add it to my watch list and hope Wall Street overreacts to a bad quarter or two down the road.

What I don’t like

Even though the stock isn’t cheap, I also think if the company continues on its current track buyers at current prices will receive an adequate return. The deal breaker for me is the CEO owns exactly zero (0!) shares of stock. He has 158,000 options that he’s yet to exercise, but even these are only worth 1.6x his 2014 income. As is so common in software/tech companies, there is also a decent amount of dilution every year via options.