Napco Security Technologies (NSSC, $5.56) is one of the companies I met with at the MicroCap Conference two weeks ago. At a quick glance, Napco appears to be a typical manufacturer with no competitive advantage and low margins, but there may be more to the story. They manufacture security products such as alarms, door locks and surveillance systems that are sold through a distributor network with schools being the major end user. They occasionally get large one-off projects like the $1.7 million dollar sale to Pepperdine University as part of the school’s larger security overhaul. As school shootings have become more common, schools will continue to beef up security. Just in 2015 there have been 52 school shootings (though six were suicides) with three of these considered mass shootings (four or more people shot). This provides a decent tailwind for Napco’s products.

Beyond the tailwind, what really interests me with Napco is their two manufacturing plants. They own both facilities which have an annual production capacity of $200 million—pretty large when you consider their trailing twelve month revenue is $79 million. This leaves a lot of room to grow and spread those fixed costs across a larger revenue base. Management claims the tipping point where their operating leverage really kicks in is $20 million per quarter. Well the proof is in the pudding and the story certainly checks out. Because schools are their biggest end user, they do most of their business in the summer while class is out. The fourth quarters of 2014 and 2015 (their fiscal year ends June) had revenues of $21.5 million and $23 million with operating margins of 13.1% and 15.1%, respectively. The other seven quarters since the beginning of fiscal 2014 have averaged $18 million in revenue with a 2.8% operating margin. Not one of those seven quarters surpassed $20M in revenue. Just getting past that $20 million per quarter hump increases their operating margins by over 4x, that’s amazing!

So the big question with this investment seems to be “when will they sustainably be making over $20 million per quarter?” At their current rate of ~5% growth it would be another 2-3 years. Management has guided to $100 million annual revenue by 2017. They’re confident the sales growth will pick up thanks to some new products such as the iBridge app below. This allows users to control various parts of their home/business (lights, A/C, etc) from an app and they can also watch live feeds of any security cameras they’ve connected. Their products are mostly targeted at commercial sales, but they do some residential as well. More of these new products will be under the Software-as-a-Service (SaaS) model which is great for recurring revenue (helps to smooth out seasonality), but it seems SaaS will never be a significant portion of revenue.

Valuation

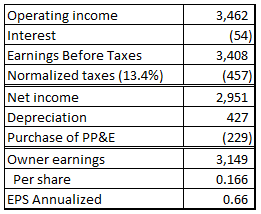

Unfortunately, the market appears to already be pricing a lot of the above into the stock. Just for argument’s sake, let’s annualize the fourth quarter of 2015 which had $23 million in revenue. Below is my calculation of normalized owner earnings for that quarter.

At a current price of $5.56 the market is valuing Napco at 8.4x their peak quarter annualized—seems pretty steep to me. My number for trailing twelve month owner earnings is $0.28, so 19.9x at the current price. If you’re wondering, their normalized tax rate is low because of international sales that are taxed at a significantly lower rate. The company has also been buying back a lot of stock but this doesn’t excite me when I don’t think the stock is egregiously cheap.

It seems like the market is already pricing in the future operating leverage so I don’t know where the margin of safety is at today’s prices. However, this is the exact type of company I like to put on my watch list and check in on every quarter. If the stock drops in the future or if the growth/operating leverage comes to fruition I’ll be able to react quickly having already researched the company.