A great business is like a great money manager. They take money in, invest it, and turn it into more money. In the case of a company, it can invest its money into manufacturing plants, marketing, hiring employees, or a variety of other things. If those investments return more money than they cost, the company’s value increases. If investments return less money than they cost, the value of the company decreases. Thus, building a successful business can be boiled down to investing money at high rates of return.

But there are only so many high return investments that a business can make. Just as finding undervalued investments became more difficult for Warren Buffett as Berkshire Hathaway grew, traditional businesses can only invest their capital at high rates for so long.

A small startup may be able to invest 100% of what it earns back into the business and generate 100%+ returns on that capital. This is how small companies can grow so fast in the beginning. But those high return investments don’t last forever and eventually that company can’t even find places to invest all of its earnings. It may continue to earn a high return on capital, but much of that is a return on previously invested capital, such as a manufacturing plant built ten years ago.

The best businesses on a look-forward basis continue to earn high returns on the capital they invest every year—incremental invested capital—as opposed to previously invested capital. This incremental invested capital is what determines how much a company’s intrinsic value increases every year. The calculation is simple:

Growth = return on incremental invested capital x investment rate

If a company earns a 40% return on the incremental capital it invests this year and it’s able to invest 30% of its earnings, the value of the company should increase around 12% (40% x 30%). The other 70% of earnings may be used to repurchase shares, pay out dividends, or accrue on the balance sheet.

This simple formula demonstrates how important return on incremental invested capital is. If a company has a high return on incremental invested capital, they should invest as much of that capital as possible. For the best businesses, growth is good.

On the other hand, a low return on incremental invested capital—say 4%—cannot be overcome by a high reinvestment rate. Investing more capital at low rates just destroys value even quicker.

The above formula also demonstrates why many of the best businesses operate at breakeven for so many years. If a company earns high returns on their incremental invested capital, the logical thing to do is invest as much of that capital as possible. It would be irrational for a business like this to voluntarily lower its reinvestment rate, thus generating earnings and forcing themselves to pay taxes—a double whammy of giving money away to the government and slowing the growth of its intrinsic value.

In summary, the best businesses can increase their value at high rates going forward. To achieve this, they must generate a high return on incremental invested capital. Thus, the most important part of determining if a company is going to have a great future is forming an opinion on their ability to continue to invest capital at high rates of return.

Unfortunately, companies that generate high returns also attract competition. And if those high returns aren’t protected by significant competitive advantages, returns will be whittled down to the cost of capital. This is the nature of capitalism. Having an opinion on a company’s future returns on incremental invested capital requires having an opinion on how durable their competitive advantages are. I categorize moats into four categories: barriers to entry, customer captivity, economies of scale, and network effects.

Barriers to entry / barriers to scale

Even though barriers to entry and barriers to scale are slightly different, I think of them as one. Some industries are very difficult to get into—those have barriers to entry. Other industries may be easier to get into at a local level but scaling to compete with the large players is very difficult—those have barriers to scale. Either way, it’s hard for a new company to compete with the large incumbent(s). Going forward, I will discuss them as one.

In my opinion, barriers to entry is the most important competitive advantage because it is the most durable. Without it, competition will never stop attacking as long as industry participants are earning above average returns. That competition may not be successful due to the other competitive advantages I’ll discuss below, but I prefer when barriers to entry prevent potential competitors from even trying. As Competition Demystified put it:

Life in an unprotected market is a game played on a level field in which anyone can join.

McKinsey’s Valuation found that unless an industry consolidates down to three or four large companies, and they are able to keep potential entrants out, competitors rarely get rational about pricing. Winning market share via lowering prices is too tempting in fragmented markets. But pricing wars generally hurt the entire industry.

In Measuring the Moat, Michael Mauboussin found that the rate of companies entering an industry has historically exceeded the rate of companies exiting an industry. This means more competition over time. And the higher returns a company generates, the more competition it attracts. High returns are generated thanks to competitive advantages, but even stronger moats are needed to keep the increasing competition at bay. Barriers to entry that don’t even allow the competition in the door is my favorite kind of moat.

A good example of barriers to entry is Amazon’s e-commerce business. They have a couple of legitimate competitors—eBay, Walmart, and Target—but starting a new general merchandiser is a monumental task. A new startup would have to attempt to overcome Amazon’s ~50% market share, their 100 million sticky Prime customers, and the billions Amazon has spent on infrastructure and logistics that is needed to run a massive e-commerce operation.

Customer captivity

Customer captivity is second on my list of competitive advantages. Captive customers struggle to stop using a company’s product or service, which means it’s hard for potential competitors to get traction. There are three reasons that customers struggle to leave a company: switching cost, habit, and search cost.

In general, I find switching cost to be the strongest of the bunch. This is a situation in which a customer would require significant time and/or money to change providers. A common example is business-to-business software-as-a-service products.

Once a dentist office signs up for a software program to handle its scheduling and customer database, switching to another provider would require a significant time investment (and probably money lost in terms of productivity). And as that software program becomes ingrained in the daily operations of that dentist office and all the employees learn how to use it, those switching costs increase over time.

Habit occurs when customers use a product or service on a very regular basis. Purchases are so habitual that they’re virtually automatic. The classic example of this is Coke. There’s no switching cost that prevents a Coke drinker from buying a Pepsi, but they rarely do. Humans are creatures of habit, so selling a product that customers purchase regularly without even thinking about it is a great situation to be in.

Search costs arise when products are complicated and thus challenging to search for. Health insurance is an easy example here. Besides switching jobs, how many times have you voluntarily changed health insurance? As long as the insurance is adequate and the company hasn’t screwed you over, it’s not worth the effort to change. Because different health insurance is difficult to compare apples-to-apples, it’s hard for a consumer to be confident in what they are switching to.

Customer captivity often results in a business that has pricing power. If customers struggle to leave, that business is going to have more control over how much those customers pay. Companies that decide on their own whether they want to raise or lower prices are in control of their own pricing destiny. Commodity businesses don’t decide for themselves to raise or lower prices—the market decides for them. Great businesses control their own pricing.

Economies of scale

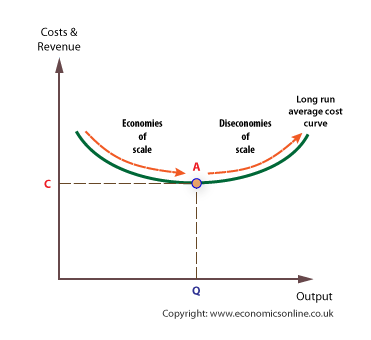

Just because a business is large does not mean it benefits from economies of scale. Economies of scale are present in industries that require a lot of fixed cost to operate in. The more fixed costs there are, the more a company can spread those costs over more units as they scale—thus lowering the per-unit fixed cost.

Why I don’t rank economies of scale higher is because their benefits usually run out. Barriers to entry and captive customers can theoretically last forever, whereas economies of scale reach a point of diminishing returns. This is because industry growth is the enemy of a company that benefits from economies of scale.

As a simple example, let’s say a niche industry requires $40 million of fixed costs to operate in and the entire industry only generates $100 million in sales. Most likely, the first mover would dominate this industry for many years. The fixed costs to compete, relative to the size of the industry, are too high for a new entrant to bother with. The incumbent has a significant competitive advantage because they’re the only ones with economies of scale in this industry.

However, if this is a growth industry that later expands to $1 billion in total sales, more competitors will be able to justify spending that $40 million upfront to compete. If the industry expands to $10 billion, suddenly that $40 million in fixed costs isn’t much of a hurdle at all in relation to the potential of the industry. Competition Demystified put it well:

if the market is sufficiently big, the share of fixed costs in each unit can become so small that the average costs stop declining. Then other companies, although their sales do not equal those of the largest firm, can come close to matching its average cost, and the advantage dissipates. Clearly, economies of scale persist only so long as the decline in fixed costs for the last unit sold is still significant. In bigger total markets, there are fewer relative economies of scale. In this sense, growth may be the enemy of profitability.

Essentially, economies of scale are subject to the law of diminishing returns. I believe we’re witnessing this right now with Amazon’s e-commerce business. For many years, they have dominated e-commerce at least in part because there are significant fixed costs in that industry, and they were the only ones with the scale to adequately cover those costs. This gave them economies of scale in purchasing and logistics. The more they sold, the more purchasing power they gained over manufacturers, and the lower prices they could negotiate.

But building out distribution is subject to diminishing returns and manufacturers can only lower their prices so much. In addition, the e-commerce industry has grown significantly over the past twenty years. In the beginning, the fixed costs required to run an e-commerce business at scale were more than the industry was even worth. Next, Amazon was finally able to cover the fixed costs, run a profitable operation, and benefit immensely from economies of scale.

Now, the industry has grown enough that, on a relative basis, the fixed costs to run an e-commerce business at scale are decreasing. This means it’s easier for competitors like Walmart and Target to compete with Amazon on price—and that’s exactly what we’re starting to see.

Network effects

Network effects happen when the value of a business increases with each additional user. Users attracting users is a fantastic place for a business to find itself in.

eBay was one of the first network effect websites to hit it big. More sellers create more value for buyers, which attracts more sellers, and so on. Because of the self-reinforcing nature of network effects, growth can explode in these businesses.

Despite that, I don’t rank network effects higher as a competitive advantage because, like economies of scale, there is a limit to their benefit. At some point, the marginal value of an additional user starts to decline. Ten years ago, my Facebook experience improved as people from my extended friend group continued to join the site. But today, basically all Americans are on Facebook and people in India joining the platform doesn’t improve my experience.

Network effect flywheels are also in danger of unwinding. Witnessing the explosive growth of a network effect platform is amazing, but they can unwind just as fast. Network effects are much more durable if the business also has captive customers. This decreases the ability of the users to leave en masse. Thus, I believe strong network effects are dependent on the business also having captive customers.

The Greatest Moat

Barriers to entry and customer captivity are almost always strong advantages on their own, but economies of scale and network effects are made much stronger when paired with other moats. Economies of scale weaken over time, but if combined with captive customers, a competitor will have a much tougher time getting enough revenue to get over the hump of the industry’s fixed costs.

Likewise, captive customers strengthen network effects. Flywheels can unwind just as fast as they wind up, but not if the business has captive customers. Because competitive advantages strengthen when they are combined, the best businesses benefit from all four:

Barriers to entry + customer captivity + network effects + economies of scale

Benefiting from all of the above competitive advantages is the best position a company can be in. Potential competitors struggle to enter the industry due to barriers to entry. Customers struggle to leave the company due to customer captivity. Current customers—who can’t leave—attract new customers due to network effects. And the bigger the company gets, the harder it is for others to catch up due to economies of scale.

Besides the above four competitive advantages, there is one other important factor that is worth mentioning when analyzing a company’s competitive position: how concentrated their customers and suppliers are.

Customer / supplier concentration

Great businesses have power over their customers and suppliers. Companies that have large suppliers are in tough spots with negotiations and thus have less control over their costs—which means less control over their pricing. Likewise, a business with a concentrated customer base is always at risk of losing an important customer.

I have witnessed how a business can crumble virtually overnight when losing a large customer. Likewise, many micro-caps have all their manufacturing done in one plant. A single fire at that plant could kill the company. These are major risks that get overlooked because they are rare. But when that risk comes to fruition, the results can be devastating.

The best businesses have a diversified customer base and are not beholden to any single supplier. Without any significant suppliers or customers, the business will be the one calling the shots.

All growth is not created equally

There are good ways to grow a business and there are bad ways. To understand the difference, there are two important factors to consider: the timing of monetary investments and how competitors will react.

On the timing of investments, developing a new product internally is less risky than acquiring a large company. Internal product development only requires investments as stages of progress are reached. Future investments can be abandoned if preliminary results are not promising. Acquisitions, on the other hand, require the entire investment to be made upfront.

On the second factor, the less competitors will retaliate against a growth strategy, the better. If a business develops a completely new product line, it’s hard for anyone to retaliate because there are no direct competitors. On the other hand, stealing market share from a direct competitor in a mature market will almost certainly result in them fighting back.

Combining the above two factors, in general the best growth strategy is (in order): develop a completely new product category, expand existing product market, increase market share in a growing market, compete for share in a stable market, and acquire other businesses.

AWS is a good example of the benefits of developing a completely new product. First, the investments to develop AWS were made gradually. If AWS was ever failing, Amazon could have abandoned the project and redirect future investments to other projects. Thus, the risk was moderated.

Second, while Microsoft Azure eventually launched four years later, AWS started the cloud compute market and had the market all to itself for those first four years. At that time, AWS was stealing business from traditional on-premise IT infrastructure. If a company wanted cloud IT, there’s not much Oracle could do about that. As I go down the list of best to worst growth strategies, it becomes easier for competitors to retaliate.

Now that AWS has a couple of legitimate competitors, their growth strategy has evolved from developing a new industry to expanding an existing industry. And in general, competitors are more friendly in growing markets as opposed to stable or shrinking markets. If AWS puts out an ad campaign that grows awareness for the entire cloud compute industry, Azure is happy because that benefits them as well.

Even if AWS steals some market share from Azure, Azure is less likely to retaliate than if the industry was mature. This is because Azure is still growing itself. Internally, Azure may not even notice losing a point or two of market share because the industry and all companies within it are growing so fast.

If an industry is mature, the only way to grow is by taking market share from competitors. But because this growth directly harms competitors, the other companies are almost certain to retaliate. When the cloud compute market is mature, Azure will notice losing a point or two of market share because that would mean revenue declines. Thus, they would be forced to retaliate against AWS.

Finally, growth via acquisitions is a very common strategy. Unfortunately, it’s also been shown to be the worst way to grow a business. Thinking about M&A from a high-level, it’s clear how bad of a bet it is. Acquisitions create value when the cash flows of the combined entities are greater than they would have been otherwise AND the premium paid wasn’t more than the increased cash flows.

According to Valuation, the average acquisition premium is 30%. This means the value of the acquired company must be increased 30% just to breakeven on the acquisition. And when it comes to acquiring public companies, the public market is reasonably efficient most of the time. Thus, the acquired company was probably fairly valued by the market prior to being purchased—and then 30% was paid on top of that fair value! And this large price has to be paid all upfront. Once an acquisition is made, there’s no way to decrease that investment risk.

Not surprisingly given the above, Michael Mauboussin determined that only around one-third of acquisitions create value for the acquirer. Those last three words are key. On average, acquisitions do create value, but most of that goes to the shareholders of the acquired company via the premium paid. So, the base rate for acquisitions is awful. But there are M&A strategies that perform better than others.

Both McKinsey and Michael Mauboussin found that the larger the acquisition, the worse the result. One issue with large acquisitions is that often the companies are already at scale, so there aren’t any scale advantages to bringing the companies together.

At some point, large businesses reach a point where incremental scale, because of diminishing returns, is not worth much. Even worse, many large companies go into a period of diseconomies of scale. This is when a company’s cost per-unit actually increases due to the inefficiencies inherent in many large companies—bureaucracy and poor communication are two of the common causes.

In addition to small acquisitions outperforming large ones, private deals also outperform public deals. For private companies, there is no public price that a premium must be paid upon. And of course, paying less is better than paying more.

Acquisition returns are also negatively correlated with the number of bidders. Buying small private companies is good. Getting into a bidding war for a public company is bad. Michael Mauboussin, in Capital Allocation, summarized his M&A findings as follows:

Deals they call opportunistic, where a weak competitor sells out, succeed at a rate of around 90%. Operational deals, or cases where there are strong operational overlaps, also have an above-average chance of success. The rate of success varies widely for transitional deals, which tend to build market share, as the premiums buyers must pay to close those deals can be prohibitive. Finally, the success rate of transformational deals, large leaps into different industries, tend to be very low.

The sustainability of a great business

As investors, it’s rare to find companies with strong organic growth, high returns on incremental capital, and multiple competitive advantages—and at an attractive valuation. But the best part about all of the above is that when you do find a great business, the evidence says they are most likely to stay great. Mauboussin suggests that,

Economic moats are almost never stable. Because of competition, they are getting a little bit wider or narrower every day.

If competition is attacking, the moat is shrinking. If competition can’t attack due to how strong the company’s competitive advantages are, the moat is widening. Valuation found evidence to support this as well:

The ROICs of the best performing companies do not revert all the way back to the median over 15 years. High performing companies are in general remarkably capable of sustaining a competitive advantage.

Finally, it’s important to note that none of the above is required. There’s probably a business out there that has dominated their industry doing the complete opposite of everything I just discussed. But it helps to understand the base rates for what determines successful businesses. Betting against a base rate requires overwhelming evidence.

There’s no getting around that businesses have to invest capital at high rates of return to be successful. To do so, they probably need several strong competitive advantages that keep potential competitors away. Finally, organic growth of new products usually outperforms other types of growth, especially large acquisitions. Those are the base rates of what makes a great business.