In 2014, Opendoor started buying and selling homes online. While many other companies have since entered this growing industry, Opendoor remains the leader in what has become known as the iBuyer market. For an extra ~$6,000 (on a $300,000 house), a homeowner can be out of their house in a week or two and avoid the normal selling process—listings, showings, dealing with a realtor, negotiating prices, and months of uncertainty.

In April 2018, Zillow entered the iBuyer market. On their Q4 conference call two weeks ago, they made it clear that their new segment, Zillow Homes, will be the main focus of theirs going forward. Not very often does an $8 billion-dollar company that dominates its niche (real estate traffic online) announce a strategic shift as big as this—especially when the new business is going to be low margin, capital intensive, and cyclical.

With that being said, Zillow makes a convincing argument as to why this potentially massive market is worth the risk. Zillow is already the go-to source for potential home buyers, home sellers, and agents. In total, Zillow.com and its affiliate websites account for almost 50% of all real estate web traffic in the US.

In the iBuyer market, this massive audience should allow Zillow to acquire customers cheaper than their competitors. And with homeowners now coming to Zillow.com to potentially sell their house, Zillow can sell many of those leads to the thousands of real estate agents who already use the site. Finally, Zillow acquired a mortgage lender in Q3 2018. Attaching mortgages to the homes that Zillow sells will increase their profit per home. By monetizing each customer more, this may allow them to lower their seller fees and/or spend more when purchasing homes.

Let’s parse through these claims. The argument for Zillow to do their own mortgage lending sounds logical. A traditional home sale results in a 6% fee paid to the realtor. On the other hand, the typical iBuyer charges a seller fee of around 7-9%. However, if Zillow earns an additional 3% by attaching the mortgage, they can decrease their seller fee to be right in line with, or even cheaper than, the traditional realtor model. Home buyers have to get a mortgage anyway, so they shouldn’t care too much if it’s through Zillow—as long as the rates are competitive.

I don’t know if this is a durable competitive advantage though. If vertically integrating mortgages with the iBuyer model results in a lower cost structure, I expect other iBuyer competitors to start or acquire a mortgage lender just like Zillow did.

The advantage that is much more difficult to replicate is Zillow’s website. Zillow is the first website people go to who are buying or selling a home. Zillow.com gets hundreds of millions of views per year and is the 29th most popular website in the US—and #1 in the real estate category (according to SimilarWeb).

Zillow’s claim is that because they have the most website traffic in the industry, they will have the lowest customer acquisition costs. Organic traffic is much cheaper than traffic that is explicitly paid for. Their iBuyer competitors like Opendoor and Offerpad are not popular websites, so they have to acquire many of their customers via online ads.

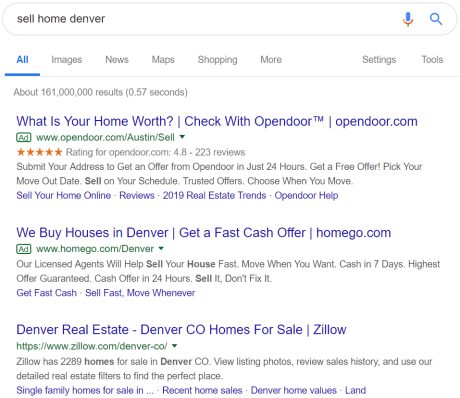

As a test of this, I Googled “sell home [city]” and “buy home [city]” in the four markets that Zillow Homes has been active in the longest—Phoenix, Las Vegas, Atlanta, and Denver. Zillow did not pay for one Google ad in those eight searches. All of the display ads were competitors—lots of Opendoor ads and then a variety of smaller iBuyers and realtors. In every search, Zillow was the first or second organic result below the ads. This is obviously a very small test, but the optics are that Zillow doesn’t feel the need to pay to attract home buyers or sellers in their most established cities. Their competitors do though.

The other advantage Zillow has is their ability to sell leads to the thousands of real estate agents who already use Zillow. Currently, Zillow receives over 300 offers every day from homeowners looking to sell, but Zillow only buys 3-4% of these houses. The rest of these offers are very high-quality home seller leads for real estate agents.

Mike Delprete wrote a great post walking through the math on seller leads, but suffice to say this by itself has the potential to generate upwards of a billion dollars in very high margin revenue for Zillow. For a company that didn’t earn a profit on $1.3 billion of revenue in 2018, that would be quite significant.

Counteracting some of the above advantages is the fact that this should always be a price sensitive market. Many e-commerce companies have struggled to earn high returns on their capital because of how price transparent the internet is. It’s hard to price a widget much above cost when customers can easily price compare several competitors against each other. I think this issue will be even more pronounced in the iBuyer market.

While few e-commerce websites benefit from customer switching costs, the iBuyer market should have even less customer loyalty. Americans stay in their homes around ten years on average, so there will be zero loyalty to any company or even method of selling a home (i.e. traditional vs iBuyer) when that time to sell comes. Even though most Americans are familiar with and have used Zillow before, there are no switching costs that are keeping them from using a competitor. And the more expensive a transaction is, the more likely customers are to price compare.

While many people aren’t going to price compare on a $20 widget they can one-click order from Amazon, virtually everyone selling a home will get multiple offers. When people are making one of the biggest financial decisions of their lives, they are incentivized to spend time researching their opportunities and trying to maximize the price they get. If another iBuyer offers a home seller $1,000 more than Zillow, why wouldn’t they take it?

On the other side, iBuyers are incentivized to make it as easy as possible for a home seller to get an offer. If the process isn’t simple, the home seller will abandon and go to the next iBuyer. That’s a bad combination for iBuyers. The final result will be multiple iBuyers that are very easy to get offers from and price compare against.

Some companies are able to overcome a lack of pricing power or customer loyalty with economies of scale. The biggest iBuyer may have a lower cost structure that allows them to underprice competitors. And currently, Zillow is several times larger than the companies that are solely focused on the iBuyer market.

Companies that benefit the most from economies of scale have large fixed costs. The more fixed costs there are, the more a company can spread those costs over more units as they scale—thus lowering the per-unit fixed cost. This is what enables large companies to have lower cost structures. A good example here is Amazon Web Services (AWS) and the massive fixed costs required to compete with their data center infrastructure.

Other industries, like the iBuyer market, have low fixed costs. Most of the expenses in this industry are variable—buying a house and doing repairs. With fewer fixed costs to overcome, it’s easier for startups to enter the industry and be competitive with the largest iBuyers on a per-unit fixed cost basis.

Low fixed costs also limit how much the iBuyer pricing can come down. Fewer fixed costs means less opportunity for economies of scale, which means less ability to lower prices in the future. Because most of an iBuyer transaction costs are variable, there isn’t as much room to lower seller fees to get them more in line with the traditional 6% realtor fee.

Like many aspects of the real estate industry, the economies of scale in the iBuyer market will be mostly local. Being the biggest iBuyer in a city will result in the most efficient use of employees when it comes to viewing homes, fixing up homes, and selling them. Having the most home inventory in one city will attract the most buyers, but that doesn’t scale to other regions.

If someone is moving from Cincinnati to Austin, they are going to visit the websites that have the most Austin home inventory. That consumer doesn’t care how much inventory an iBuyer has in Denver or Jacksonville. And the person who sells their house to Zillow just wants to get the most money. I don’t think there are strong network effects here where more buyers bring more sellers, which then brings more buyers and so on.

The biggest iBuyer will probably own tens of thousands of homes across the US. That requires a significant amount of money and inventory management, so it’s tempting to think there are large barriers to entry. But because most of the economies of scale are local, the barriers to entry and barriers to scale are also local. Thus, the largest iBuyer should still have legitimate competitors in each city they operate in—even if they are different competitors. A small iBuyer won’t require national scale to compete at a local level.

Earning excess returns in a transparent, price competitive market requires either having the lowest cost structure or being able to monetize customers in ways that competitors can’t. If Zillow can acquire home buyers and sellers cheaper than their competitors, Zillow will have a lower cost structure that they can use to underprice the competition. Likewise, if Zillow is able to monetize iBuyer customers more than their competitors via seller leads, Zillow’s profit per deal will be substantially higher.

The combination of lower customer acquisition costs and increased monetization per customer could potentially be deadly. If both come to fruition, Zillow can underprice other iBuyers on their seller fee and/or pay more per house than their competitors can afford. It’s even possible that Zillow pays full market price for homes and earns enough just from selling the high-quality leads to agents. In this scenario, I’m not sure how others could compete. No one else owns almost 50% of all real estate web traffic that includes home buyers, home sellers, and real estate agents.

However, if Zillow is forced to pay for customers, or their competitors get enough local traffic organically, Zillow may not be able to earn high returns on capital in this new segment. If seller leads don’t pan out, or if those leads simply cannibalize Zillow’s traditional premier agent business, they may monetize customers at the same rate as other iBuyers. In this scenario, Zillow would simply be one of many in a commoditized industry.

Zillow is going after a low margin, capital intensive business in a cyclical industry that has price transparency and zero customer loyalty. But Zillow does have two potential advantages: lower customer acquisition costs via their web traffic and increased customer monetization via seller leads. I agree with their CEO, Rich Barton, that Zillow is taking a “big swing” on the iBuyer market.