When investors bring up Lemonade’s decreasing book value, there are generally three concerns: regulatory risks, growth constraints, and valuation. I am going to address all three.

1. Regulatory risks

The risk-based capital ratio is the single formula that insurance regulators care most about. Risk-based capital is the regulator’s shorthand for how much capital an insurer is required to have on hand. The “risk-based” part of this title is important: it is risk-adjusted. All things being equal, a riskier insurance company requires more capital.

At yearend 2025, Lemonade’s US risk-based capital was $38.6 million. If an insurer’s statutory capital falls to 200% of its risk-based capital (so $77.2 million in Lemonade’s case), the insurer must submit an action plan on how it will fix its capital position. If the risk-based capital ratio continues to fall, regulators get more involved and will take control of the insurer if its ratio drops to 70%.

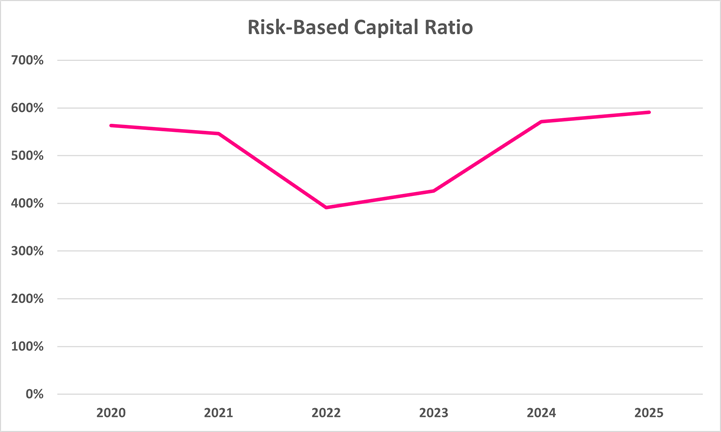

With that in mind, let’s see how Lemonade’s risk-based capital ratio has trended since IPO.

Generally, anything above 300% means regulators are happy and the insurer is nowhere near having regulatory issues. Lemonade far exceeds that 300% threshold, ending 2025 at 591%.

Given that, why do investors point to Lemonade’s decreasing book value as a regulatory risk? One, misunderstanding. Book value and book value per share have been decreasing for years—even as their regulatory metrics have remained very healthy. This by itself should tell you there is more to regulatory risks than simple book value. But two, decreasing book value could theoretically be a leading indicator of risks to come.

If Lemonade were expected to lose money for many more years, and they didn’t have the Synthetic Agents program, their cash would decrease and their risk-based capital requirements could increase enough to be a problem. But this is very unlikely.

Today, Lemonade has $1 billion in cash and are net cash flow breakeven thanks to the Synthetic Agents program that covers 80% of their customer acquisition costs. I have done my own math on the Synthetic Agents program and I think it is great for both Lemonade and their partner General Catalyst. General Catalyst seems to agree given they expanded the original partnership on the same terms for another $200 million for 2026. So, I do not think this deal is going anywhere in the near-term (eventually Lemonade will probably want to own more of their unit economics).

As of yearend 2025, Lemonade has $277 million in statutory capital and surplus for their US business. That capital and surplus grew 33% in 2024 and 26% in 2025. With over $1 billion of total cash at the company level, Lemonade has ample room to grow as is. Even more, they should be GAAP income profitable by yearend 2027, so total cash will start to increase then.

With that being said, I will not be surprised if Lemonade’s risk-based capital ratio does deteriorate some in the near-term. Up until June 2025, Lemonade was using reinsurance for 55% of its premiums. Now, they are in the middle of a 12-month transition to only ceding 20% to reinsurers. As Lemonade keeps more of its premiums to itself, its risk-based capital requirements may increase.

In addition, management has made it clear they are going to start increasing loss ratios to be even more price competitive. First, this is massively bullish. I discussed in my original Lemonade writeup in 2023 why I believe their moats could result in a more efficient business than their large competitors. And lower expense structure = lower prices. This is the first evidence of that.

Given their gross loss ratio ex-CAT was 60% or less every quarter in 2025, I think they have plenty of room to profitably lower prices to win more business. Management’s quotes on this dynamic from their Q3 2025 results were very insightful.

Lower prices worsen gross margins and loss ratio, yes, but the attendant boost in revenue often more than makes up for that. This means that for some parts of our business a higher loss ratio and slimmer gross margins will translate into higher gross profit. Given the choice, we will always privilege dollars over percentages… In pursuit of maximizing gross profit dollars, there will be segments where we will let loss ratio rise because the elasticity of demand is such that, that will spike demand and retention in a way that offsets the margin becoming a little bit more constrained

You can envisage a situation where we could lower prices so dramatically where we would be profitable with a 90% loss ratio. The math here and the degrees of freedom that we have is pretty dramatic and something that will be very, very hard for the incumbency to replicate. So, we are using the data to guide us in terms of what is optimizing gross profit. At times, that will mean selling a lot more with thinner margins, at times not. Some of our products are more price elastic, some are less, some campaigns are more elastic, some are less… But we’re thinking about loss ratio less as one big aggregate number with a target [and] more as fine-tuning by product, by campaign, by region, and that will result in different loss ratios, different product lines but always in the service of maximizing gross profit.

On the other hand, Lemonade’s CAT exposure has come down significantly over the past few years. They have non-renewed and reduced exposure in their home insurance segment, especially in high-risk regions with hurricanes and fires. Less CAT exposure means a less risky business.

In short, Lemonade’s current risk-based capital ratio is *291%* higher than it needs to be before regulators are likely to show any concern. There are some puts and takes to this number over the short-term, but what matters is they have at least several years of runway in their current state. And they are about to reach profitability in 2027, so their current state is about to improve dramatically.

And frankly, raising a few hundred million dollars would not be a big deal given this company’s upside, but management has reiterated many times they will not need to raise money again. And I’ve followed Lemonade long enough to trust the two co-founders when they say that.

2. Growth constraints

Despite Lemonade’s reinsurance change from 55% to 20%, management estimates their premium to capital ratio remains around 6:1. This means they can write about $6 of gross premium for every $1 of total adjusted capital they have. Now, total adjusted capital is not a GAAP reported number, but statutory capital and surplus of their US insurance subsidiaries is a good enough estimate (Europe is only 5% of their business). As an estimate this is likely a little low, but I’m happy to be conservative.

At a 6:1 ratio and expected gross written premiums around $1.9 billion in 2027, Lemonade would need capital and surplus of ~$320 million next year. That is only 16% more than their 2025 balance of $277 million (what I am conservatively using for total adjusted capital).

Given their investment income (>$20 million three straight years), reserve development (positive for 6-straight years), and cash available for capital contributions, growing capital and surplus by $43 million to be able to handle their expected business in 2027 does not look like a concern at all. For reference, they grew capital and surplus by 33% in 2024 and 26% in 2025. And then after 2027 they will be GAAP profitable with a growing book value, so all of this becomes easier.

Overall, I see very little risk in Lemonade’s growth being constrained due to book value or regulatory issues.

3. Valuation

All companies are valued based on the market’s estimate of their future free cash flow discounted back to today. Insurers included. For mature insurers with mature growth rates, book value can be a reasonable proxy to use for valuation. But similar to price to earnings, book value is a shorthand valuation method that makes a lot of implicit assumptions about a company’s future.

Comparing Lemonade’s price to book value today to Progressive and other insurers makes no sense. Progressive is *eight decades* ahead of Lemonade in its growth curve. From a valuation perspective, Lemonade is not comparable to their large competitors.

Lemonade is currently growing >30% and is expected to continue that rate for at least the next five years. If successful, Lemonade’s runway to grow at double-digits will be measured in decades. Progressive was founded in 1937 and its net premiums earned still grew 10% in 2025. Plus, Lemonade is about to flip to profitability. Companies growing 30% with long runways for growth that are on the verge of profitability deserve to sell for high multiples.

If an investor is determined to compare Lemonade to incumbents, a more logical comparison would be to look at what fair value should have been for Progressive when it was a ten-year-old company like Lemonade is today. But Progressive did not IPO until 1971, so that is the best we can do.

As a fun exercise, I got ahold of Progressive’s first annual report from 1971, 34 years after it was founded. That first annual report came out in March 1972 when Progressive’s stock was selling for around $18 per share (numbers not adjusted for stock splits). With $8.91 per share of book value, Progressive was selling for 2x book.

Progressive’s 54-year CAGR since then is 20.3% (including dividends). If instead of paying 2x book value for Progressive in March 1972 you paid 20x book, you still would have earned 15.2% per year—pretty incredible for 54-years! That compares to the S&P 500 54-year return of 11%.

Now, obviously there is major survivorship bias and hindsight bias here! I am not suggesting investors back then should have been willing to pay 20x book to invest in Progressive. My point is that any investor who compares Lemonade’s valuation today to Progressive’s valuation today is not making an apples-to-apples comparison.

When Progressive IPOed *34 years* after its founding, it could have been priced at 10x book and still generated 16.7% returns for the next 54-years. With hindsight, 10x book was very undervalued. So was 20x. Incredibly, fair value—with hindsight!—was around 150x book value! Long runways of profitable growth are immensely undervalued by investors.

But honestly, that little exercise is mostly meaningless. All companies are valued based on estimates of their free cash flow discounted back to today. In my opinion, reasonable discounted cash flows for Lemonade result in a fair value that is 2-3x today’s price. Relative valuation does not factor into my valuation at all.

Final thoughts

Lemonade management has a lot of control over how fast they grow. They have little market share in almost all their products and regions. Growth is only capped by marketing expenses and regulatory capital requirements.

In late 2022, their base case target for positive EBITDA was mid-2026. They eventually changed that to the current target of Q4 2026—though I won’t be surprised if it’s Q3—but nonetheless, that is pretty damn good for guiding four years out.

Given the predictability of their business, I don’t think it is a coincidence that they are going to hit GAAP profitability with 1-2 years of cushion before their surplus capital requirements become a limiter on growth. This has been planned for years.

For Lemonade, growth and near-term profitability are opposing forces, kind of two sides of a seesaw. Growing faster results in customer acquisition costs that get expensed immediately, hurting near-term profitability, while the corresponding revenue is earned over years. As long as they are acquiring customers with good unit economics, growing faster increases the enterprise value of the business even if near-term profitability is hurt.

However, they are also an insurance company, so fast growth that pushes out profitability has to be balanced with regulatory and capital requirements. At some point, they need to be profitable to grow book value, otherwise they would have to rely on outside capital to fund growth, which is not sustainable long term.

Lemonade last raised money in 2021, and management has repeatedly said they don’t plan to raise money again. With that $1 billion capital base from 2021, their goal should have been to maximize growth with great unit economics for as long as possible and then to turn profitable in time that their capital base starts to grow and negates the need to raise more money. Plus, a little cushion to be safe.

And five years later that is exactly what is about to happen. I believe management has done a very good job to maximize the enterprise value of the business with that $1 billion of capital while also balancing the need to reach profitability. As I’ve described in numerous writeups, including my December one, I think the Lemonade co-founders are vastly underrated when it comes to their capital allocation skills.