David Winters, CEO of Wintergreen Advisers, has now written two letters in the past six weeks to Consolidated-Tomoka’s board of directors. The first letter was relatively tame and requested a shareholder vote at the 2016 annual meeting to put the company up for sale. Winters feels the market is not accurately valuing CTO (spoiler alert: I agree) and some combination of a sale and/or liquidation would maximize shareholder value. Winters’ second letter to the board made some serious claims: “we believe that CTO management, led by John Albright, is actively trying to deceive shareholders with filings, investor presentations and disclosures that obfuscate, confuse and hide what is really going on at CTO.” Not surprisingly, the stock dropped around 10% that day and has since recovered about half that. I want to go through that second letter point by point and give my opinions on the issues it brings to light.

The letter starts out by saying “We believe CTO management violated both the letter and spirit of multiple laws”—those being the Sarbanes-Oxley Act of 2002, Securities Act of 1933, and Securities Exchange Act of 1934. These laws “require ongoing forthright and complete disclosure of material financial and non-financial information… We believe CTO’s recent public filings have not met the standards set forth in these federal securities laws.” Winters breaks the letter into three sections covering his main concerns: CTO’s use of and disclosure regarding leverage, CTO’s calculation of leverage, and CTO’s securities and derivatives portfolios.

CTO’s Use of and Disclosure Regarding Leverage

“CTO’s long-term debt has increased 44% in 2015 and over 135% since the beginning of 2014… we believe it puts the entire Company at risk.”

On the first point, Winters is correct. CTO has been increasing its use of long-term debt ever since John Albright took over in 2011. This should be of no surprise to any shareholder though as it’s been Albright’s stated plan all along. CTO is selling off their (now) 10,341 acres and growing their portfolio of income-producing properties. They’re able to use the land proceeds to purchase properties, but this is still capital intensive. CTO’s sources of long-term debt are a $75 million revolving credit facility, a $75 million convertible note, and three mortgage notes that are non-recourse and secured by specific income properties. These mortgage notes all have low rates and the first comes due in 2018.

The credit facility is the only source of debt that has traditional debt covenants and CTO is well within compliance. This credit facility does have full recourse to CTO, but it is also secured by specific properties and only has $19.5 million outstanding (which accounts for 12.59% of total outstanding debt). The convertible notes don’t have traditional debt covenants that would cause default like most credit facilities do. As long as CTO pays the annual interest on time they’re good to go. They also have flexibility in whether they pay the principal of the convertible back in cash, stock, or a combination of both.

Overall, their credit facility and mortgage notes are secured by specific properties and the convertible is covenant-light and has a lot of flexibility when it comes time to pay it off. The mortgage notes are also non-recourse to the company. Based on the current levels of debt outstanding, annual interest payments going forward should be around $6 million. Including the recently announced deals, pro forma cash and securities levels should be around $42 million. Add this to future cash generated from operations and I don’t think they’ll be in danger of being unable to service their debt any time soon.

“Based on CTO’s most recent Form 10-Q, it appears that CTO is making long-term commitments with short-term borrowing, which exposes shareholders to interest rate risk.“

As of the latest 10-Q, their 41 income properties had an average remaining lease of around 8.6 years. The convertible notes are fixed at 4.5% and are due in 2020. The mortgage notes have low fixed rates (3.655%, 3.67%, and 4.33%) and are due in 2018, 2023, and 2034, respectively. The credit facility (which only accounts for 12.59% of total outstanding debt) bears a floating interest rate that maxes out at 30-day LIBOR + 2.25% and matures in August 2018 (with an option for a 1 year extension). The fed recently raised interest rates, but they were also very clear about future increases being gradual and the overall rates remaining low for the foreseeable future. Even so, CTO says “a hypothetical change in the interest rate of 100 basis points (i.e., 1%) would affect our financial position, results of operations, and cash flows by approximately $195,000.” In my eyes, that level of interest rate risk is immaterial.

“Further, Item 303 of Regulation S-K requires that a company disclose a description of any known trends or uncertainties that it reasonably expects will have a material impact on its business. Here, we believe it is clear that CTO’s increased use of leverage represents a continuing trend and we question how anyone could take the view that a company which increases its leverage to such a degree would not expect that increase to have a material impact on its business.”

The following statement is in CTO’s third quarter 2015 10-Q: “Our long-term debt balance, at face value, totaled approximately $154.9 million at September 30, 2015, representing an increase of approximately $51.0 million from the balance of approximately $103.9 million at December 31, 2014. The increase in the long-term debt was primarily due to the $72.4 million funding received from the Notes offset by net payments on our revolving credit facility of approximately $24.0 million.” Similar statements can be found in the first and second quarter 10-Qs. CTO is not hiding the trend of increasing debt.

Item 303 of Regulation S-K states “Where the interim financial statements reveal material changes from period to period… the causes for the changes shall be described if they have not already been disclosed.” In my opinion, the quoted two sentences in the previous paragraph satisfy this requirement. I suppose CTO could explicitly lay out the reasons for the increasing leverage following those two sentences, but I don’t feel this is necessary to an understanding of the company because this information can be gathered from other areas of that 10-Q, in addition to other releases.

The 2014 10-K states “The increase in the long-term debt was due to our investment activities, including the acquisition of income properties and the investment in commercial loans.” CTO is also clear about their desire to continue this trend as the following risk factor has appeared in the 2012, 2013 and 2014 10-Ks: “Our future success will depend upon, among other things, our ability to successfully execute our strategy to invest in income-producing assets.” Likewise, the following statement is in the 2014 10-K in reference to their commercial loans: “We expect to fund these acquisitions utilizing available capacity under our credit facility, cash from operations, proceeds from the dispositions of non-core income properties or transactions in our land assets, which we expect will qualify under the like-kind exchange deferred-tax structure, and additional financing sources. We may obtain unsecured debt financing in addition to our credit facility which could decrease our borrowing capacity on the credit facility.” In my opinion, CTO has given investors enough information to understand why their use of leverage is increasing.

CTO’s Calculation of Leverage

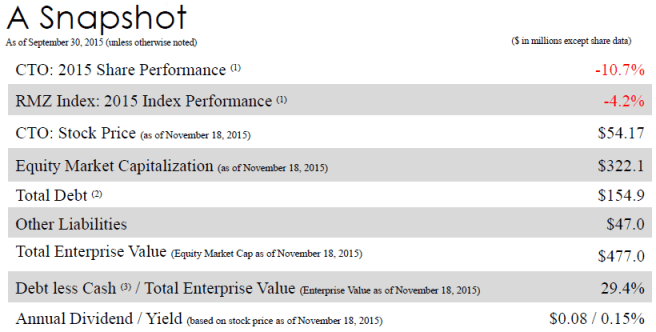

“In a November presentation, CTO management chose to present leverage ratios against ‘Total Enterprise Value.’ To us, this appears to purposefully understate CTO’s true use of leverage in order to justify increasing leverage… If measured against CTO’s Equity Market Capitalization from the same presentation, CTO’s leverage would be an alarming 48%, which could force CTO to sell off its most valuable assets at a steep discount if it is unable to service its debt.”

One of my holdings, Navigator Gas (NVGS), actually has a debt covenant from their lender that is measured by net debt to total enterprise value. I’ve seen this exact covenant in other companies as well. If lenders view this as a valid metric to measure leverage, I think it’s perfectly reasonable for companies to present it that way as well. To the second point about total debt to equity market capitalization being a better representation of leverage, on the very same slide Winters refers to from their November presentation, CTO lists equity market capitalization and total debt right next to each other (the slide is copied below). If total debt to equity market capitalization is such a damning ratio and management is actively trying to avoid presenting leverage in that way, I doubt they’d put the two numbers next to each other.

While a 48% total debt to equity market capitalization ratio is certainly high, this doesn’t necessarily correlate to their ability to service debt. As stated earlier, with around $6 million of annual interest payments going forward and pro forma cash and securities levels around $42 million (plus future cash generated from operations), debt service should be not an issue.

Next, Winters referenced an Albright quote about internal measures of net asset value not lining up to the market’s valuation and then stated, “We believe Mark Patten’s [CFO] e-mail disclosure that CTO is using hypothetical metrics to measure net asset value is also material. If CTO were to include these hypothetical metrics to measure net asset value in its financial reports without certain clarifications, we believe it could violate various provisions of Sarbanes-Oxley, including Regulation G which states that a company that presents a non-GAAP financial measure is required to compare such measure with the most comparable financial measure that is calculated in accordance with GAAP. In our view, failing to provide such a comparison prevents shareholders from accurately assessing CTO’s leverage.”

First, I believe any valuation of any company involves hypothetical metrics. Second, why would CTO’s internal measures of net asset value be subject to Sarbanes-Oxley and GAAP accounting? Especially when the internal calculation is only referred to at a high level without detail. Management teams broadly discuss internal valuations of their own companies on a regular basis.

CTO’s Securities and Derivatives Portfolios

“CTO has recently dramatically expanded an investment portfolio and initiated a derivatives portfolio, with extremely limited disclosure to shareholders.”

At yearend 2014, CTO’s portfolio of investment securities was on the books for $821,436. As of September 30, 2015, this had grown to $7,867,077. A near 900% increase certainly qualifies as a dramatic expansion, but it’s important to put this in perspective. CTO’s total assets are $333,357,568, putting the investment securities at 2.36% of assets. If every single one of their securities investments went to zero, it would have basically no effect on the company’s value going forward (besides drawing serious doubt to Albright’s stock picking abilities). My current calculation of net asset value decreases by $1.34/share if the investment securities are eliminated.

In reference to the level of disclosure, I’ll admit I don’t know what exactly is required here. It is common for companies with spare cash to have some of it invested in equity or debt securities and CTO’s disclosures appear to be on par with many other companies I look at.

“We believe that CTO’s management is trading this blind pool with borrowed money.”

While I can’t be sure, it does appear CTO is using proceeds from the $75 million convertible note to invest in securities. At yearend 2014, CTO’s cash balance was just under $1.9 million with another $821k invested. In the first quarter of 2015, CTO generated negative operating cash flow and negative investing cash flow, yet had $5.4 million invested by quarter’s end. The only major source of cash during this period was proceeds from the convertible note.

While it’s not ideal to raise money at 4.5% only to invest it in securities, I’d prefer this money sit in some investments that have a positive expected value rather than in cash earning nothing. Then when income properties come available, the securities can be sold and the cash put to its intended use. I don’t see anything in the convertible indenture that bars CTO from using the proceeds to invest in securities.

“Under Item 305 of Regulation S-K, a company is required to disclose in its Form 10-Q, material qualitative and quantitative information about the market risk inherent in the financial and derivative instruments that it trades, including the primary market risk exposures and how they have changed in the past year and how they are managed.”

I agree with Winters here. In the 2014 10-K there are no risk factors that directly discuss the investment securities. In the three 10-Qs released since (which is when the securities portfolio really ramped up), no risk factors have been added that reference the new investments.

That concludes what I feel are the most important points of Winters’ second letter to the board. Now I want to specifically discuss Wintergreen Advisers a little more.

David Winters and Wintergreen Advisers

David Winters published the Wintergreen Advisers 2014 shareholder letter on March 2, 2015. His first letter to the board was filed on November 23, 2015. The below comments are taken directly from the Wintergreen Advisers shareholder letter which came just eight months and 21 days before Winters’ first letter to the board:

“The real estate market in Daytona Beach is bouncing back, and the actions taken by CTO’s management team and board over the past four years have put the company in position to benefit from this rebound.”

“This progress at CTO has not gone unnoticed by investors. Since the board appointed John Albright as CEO in 2011, CTO shares have risen by 22% annually as of the date of this letter, far outpacing the 16% annual gain for the S&P 500.”

“Wintergreen’s actions at CTO separated the Chairman and CEO positions, gave investors an annual say-on-pay vote (before it became a requirement), and put a strong lineup of directors on CTO’s board. The board in turn hired a very capable management team, which has transformed the company into the profitable and growing enterprise it is today. We believe the best is yet to come for CTO.”

“CTO has righted its ship and is busy growing shareholder value.”

Quite a difference of opinion in a little under nine months. So what’s changed? Since Winters’ shareholder letter, CTO has increased debt (mainly via the $75 million convertible note) and ramped up their securities portfolio. I won’t rehash the entire investment thesis, but in my opinion CTO has also meaningfully grown the value of the company in that time period, as I describe in my first write-up back on August 31, 2015. Unfortunately, the market has not agreed. On March 2, 2015 (the day Winters published his 2014 shareholder letter), CTO’s stock closed at $58.84. On November 20, 2015 (the last trading day before Winters published his first letter to the board), CTO’s stock closed at $54.56, for a return of -7.27%. In that same time period, the S&P 500 returned -1.26%. Frustrating.

My knowledge of Wintergreen Advisers is limited to what is made public on their websites (1 and 2) and through sites like Dataroma that track large money managers. With that being said, according to Wintergreen Fund releases, they had $1.75 billion net assets under management at yearend 2013, $1.48 billion at yearend 2014, and $953 million on June 30, 2015. Declining assets under management often requires liquidating positions.

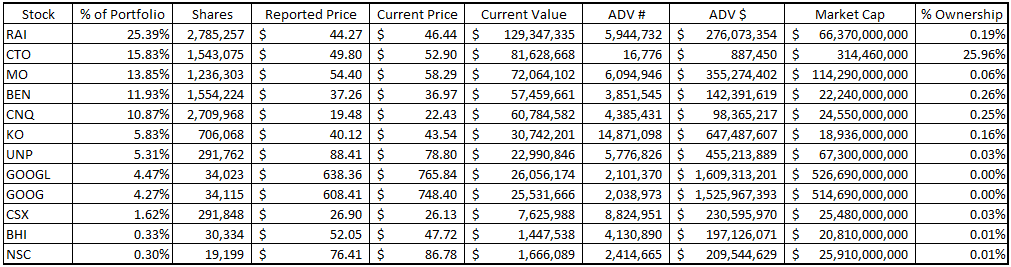

Just because of declining assets, CTO has gone from not a top ten holding at yearend 2013 to the ninth largest holding at yearend 2014 and the second largest holding at June 30, 2015 (with no buys or sells). As of September 30, 2015, Wintergreen Advisers owns 12 US stocks, detailed below (click to enlarge).

Note: This is only their US holdings but the below points I’m trying to make are unaffected by their international holdings. The first four columns are taken directly from Dataroma information. The other numbers are pulled off Yahoo Finance as of 12/25/15 (yes, this is how I’m spending my Christmas). If you study the above chart for a minute, I think there are several important things to take note of:

- CTO is Wintergreen Adviser’s second largest position.

- CTO is by far the smallest company they own. CTO’s market cap is $314 million vs the next smallest at $18.9 billion.

- CTO has by far the lowest average daily volume (ADV), both in number of shares and value of shares traded. Over the past three months, CTO’s ADV has been 16,776 shares (equivalent to $887,450).

- Wintergreen Advisers owns 25.96% of CTO (according to filings, Wintergreen Advisers owns 26.1%). The next largest percentage of a company they own is Franklin Resources (BEN) where they own 0.26%.

Excluding CTO, Wintergreen Adviser’s ownership in every one of their stocks is valued at less than one day’s worth of that stock’s ADV. This means Winters could most likely sell every other position within a few days if absolutely necessary. On the other hand, the value of Wintergreen Adviser’s CTO position is 91.98x the ADV of CTO. To say it would be difficult for them to get out of their CTO position in the open market is an understatement.

Taking it all together, Wintergreen Advisers has seen declining assets under management since 2013 and their second largest position, CTO, is far more illiquid relative to all their other positions. With such a large stake in the company, the easiest way to get out of their position would be a private deal (to a hedge fund, perhaps) or through a sale and/or liquidation of CTO. Winters owns 26.1% of CTO shares so he needs another 24% of shares to vote alongside him at CTO’s 2016 shareholder meeting this spring to force a sale. However, we may not have to wait for a vote at the annual meeting as CTO’s board is already exploring strategic alternatives, including a potential sale of the company. It sounds like we’ll know more after their January board meeting.

Nice, thoroughly written Blog. Winters probably won’t be happy now that more people know HIS decline in market performance and activity. This email has been sent from a virus-free computer protected by Avast. http://www.avast.com

LikeLike

Excellent write up. Do you think Winters may give up and start selling shares at a loss? That can substantially impact the price.

LikeLike

Well anything’s possible, but I think that’d be last resort only if his fund’s redemptions force him out of CTO and he’s already exhausted all other options. Even if he did attempt to sell a large block in the open market I’d be happy to buy more shares at a lower price so I don’t think that’s a bad scenario in the long run. Depending on what CTO announces after their next shareholder meeting with respect to the “strategic alternatives,” I won’t be surprised if Winters continues issuing 13Ds trying to force a sale. There are definitely a couple scenarios that could result in lots of short-term volatility.

LikeLike